In today's financial landscape, the term "credit score" is thrown around frequently, but what does it really mean, and why is it so crucial? A credit score is a numerical representation of your creditworthiness, calculated based on your credit history. Lenders use this score to evaluate the risk of lending you money, making it a pivotal factor in securing loans, credit cards, and even favorable interest rates.

Understanding the intricacies of your credit score can be empowering. It allows you to take control of your financial future, opening doors to opportunities that might otherwise be closed. A high credit score can lead to lower interest rates, better loan terms, and more credit options, while a low score can limit your financial opportunities. With such a significant impact, it's essential to comprehend what constitutes a credit score, how it's calculated, and how you can improve it.

In this article, we will delve into the details of what a credit score is, how it affects your financial life, and the steps you can take to maintain or improve it. We will also address common questions about credit scores, providing you with a comprehensive understanding of this critical financial tool.

Table of Contents

- What is a Credit Score?

- Why is a Credit Score Important?

- What Are the Components of a Credit Score?

- How is a Credit Score Calculated?

- How Can You Improve Your Credit Score?

- Understanding Credit Reports

- Are There Different Types of Credit Scores?

- What Impacts Your Credit Score?

- Credit Scores and Loan Approval

- Credit Scores and Credit Cards

- How Do Credit Scores Affect Interest Rates?

- The Importance of Monitoring Your Credit Score

- Common Myths About Credit Scores

- FAQs About Credit Scores

- Conclusion

What is a Credit Score?

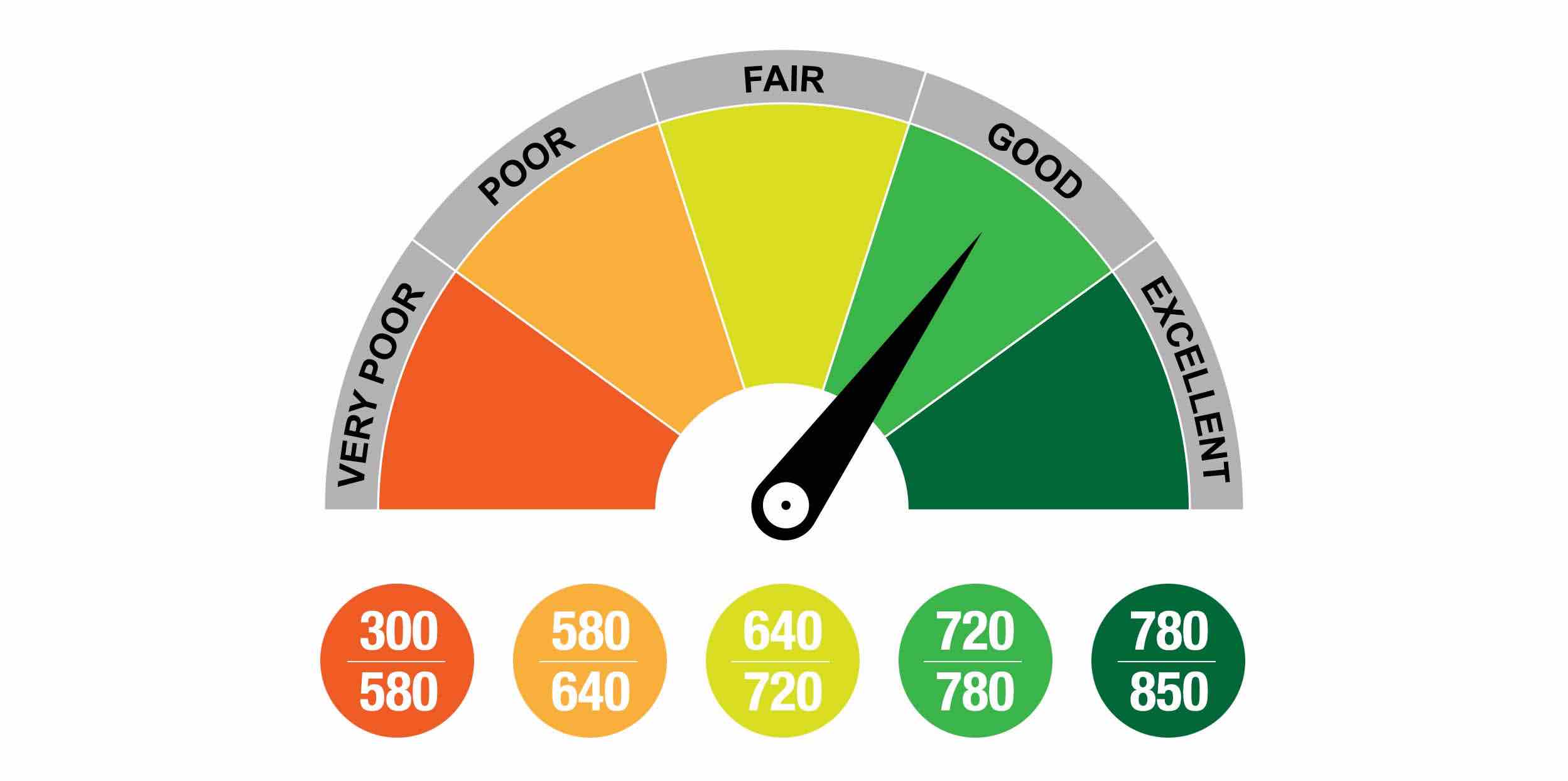

A credit score is a numerical value that represents a person's creditworthiness, calculated based on their credit history and financial behaviors. Ranging from 300 to 850, this score gauges the likelihood of a borrower repaying a loan.

Credit scores are typically calculated using algorithms created by major credit bureaus such as Experian, TransUnion, and Equifax. These algorithms consider various factors, including payment history, credit utilization, length of credit history, types of credit, and new credit inquiries.

Knowing your credit score is crucial as it can influence your ability to secure loans, credit cards, rental agreements, and even employment opportunities. A higher score indicates a lower risk to lenders and can result in more favorable borrowing terms.

Why is a Credit Score Important?

The significance of a credit score cannot be overstated, as it affects numerous aspects of your financial life. Here's why it's important:

- Loan Approval: Lenders use your credit score to determine your eligibility for loans and the terms they will offer.

- Interest Rates: A higher credit score can qualify you for lower interest rates on loans and credit cards, saving you money over time.

- Rental Agreements: Many landlords check credit scores to assess the reliability of potential tenants.

- Employment Opportunities: Certain employers review credit scores as part of their hiring process, especially for roles involving financial responsibilities.

Overall, maintaining a good credit score is essential for achieving financial stability and accessing various financial products.

What Are the Components of a Credit Score?

Credit scores are derived from several key components, each contributing to the overall score. Understanding these components can help you manage your credit more effectively:

- Payment History (35%): This is the most significant factor, reflecting whether you've paid past credit accounts on time.

- Credit Utilization (30%): This measures the amount of credit you're using compared to your credit limit. A lower ratio is better.

- Length of Credit History (15%): A longer credit history can positively impact your score, as it shows experience with managing credit.

- Types of Credit (10%): A mix of credit types, such as credit cards, retail accounts, and installment loans, can benefit your score.

- New Credit (10%): Opening many new accounts in a short period can damage your score, as it may suggest financial instability.

By focusing on these components, you can work towards improving your credit score over time.

How is a Credit Score Calculated?

The process of calculating a credit score involves complex algorithms that evaluate the components outlined above. While each credit bureau may use a slightly different model, the general approach is similar. Here's a breakdown of how a credit score is typically calculated:

- Data Collection: Credit bureaus gather information from various financial institutions, including banks and credit card companies.

- Factor Evaluation: The collected data is analyzed based on the five key components: payment history, credit utilization, length of credit history, types of credit, and new credit.

- Scoring Model Application: The bureau applies its scoring model to generate a numerical score, reflecting the borrower's creditworthiness.

While the precise calculations may vary, understanding these steps can give you insight into how your financial behaviors influence your credit score.

How Can You Improve Your Credit Score?

Improving your credit score takes time and effort, but it's a worthwhile endeavor. Here are some strategies to help you boost your score:

- Pay Bills on Time: Consistently paying your bills by their due dates is crucial for maintaining a good credit score.

- Reduce Credit Card Balances: Aim to keep your credit card balances low relative to your credit limit.

- Avoid Opening Too Many New Accounts: Each new credit inquiry can temporarily lower your score, so be selective when applying for new credit.

- Check Your Credit Report: Regularly review your credit report for errors and dispute any inaccuracies you find.

- Maintain Older Credit Accounts: Keeping older accounts open can positively impact your credit history length.

By implementing these strategies, you can work towards achieving a higher credit score and improving your financial standing.

Understanding Credit Reports

A credit report is a detailed record of your credit history, compiled by credit bureaus to evaluate your creditworthiness. It includes information such as your payment history, credit accounts, outstanding debts, and recent credit inquiries. Here's why understanding your credit report is essential:

- Accuracy: Ensuring the information on your credit report is accurate can prevent errors that might negatively impact your credit score.

- Dispute Resolution: If you find inaccuracies on your report, you have the right to dispute them with the credit bureau to have them corrected.

- Monitoring Progress: Regularly reviewing your credit report can help you track your progress as you work on improving your credit score.

Obtaining a free copy of your credit report annually from each of the three major credit bureaus is a good practice to ensure you're on top of your credit health.

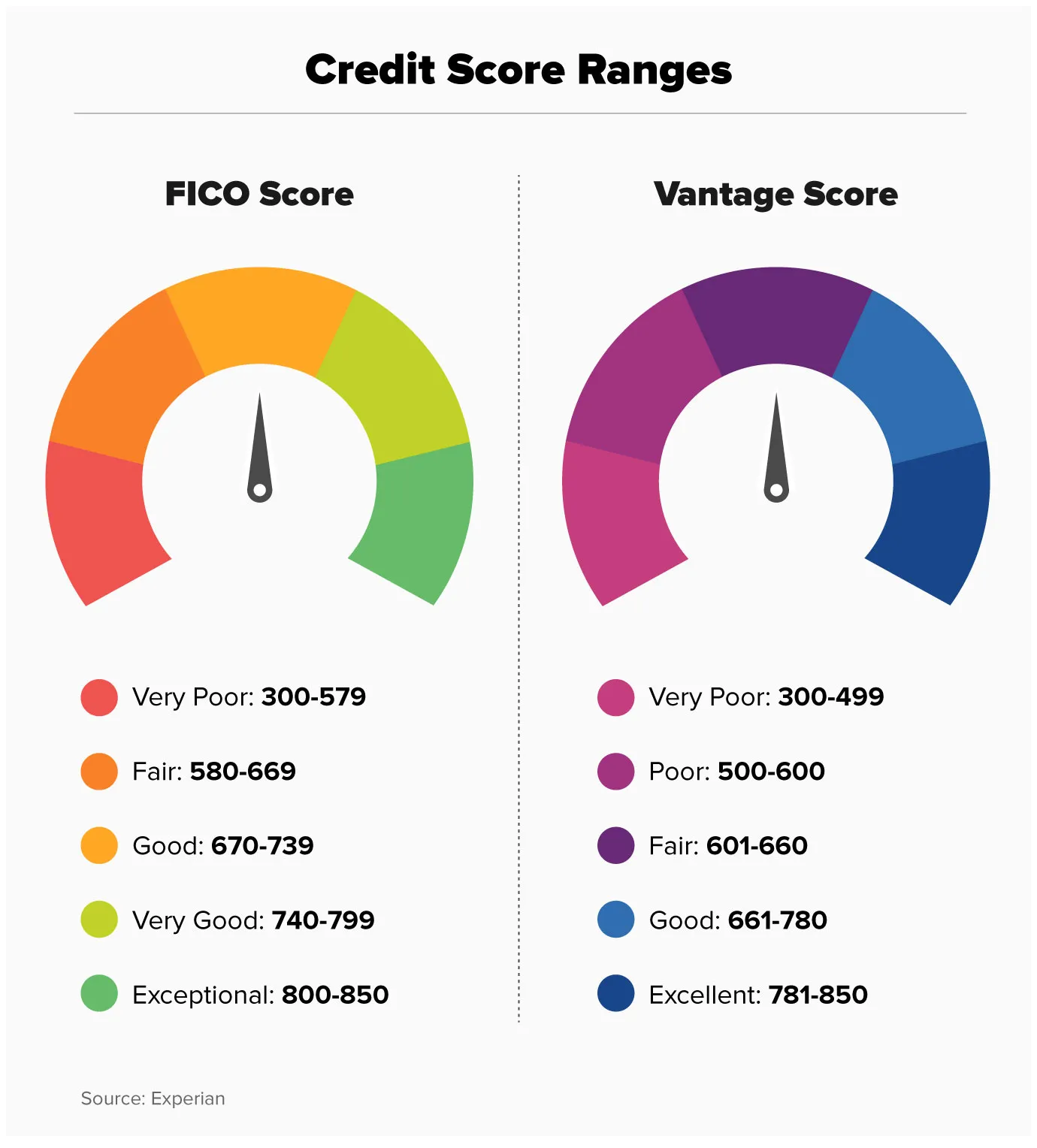

Are There Different Types of Credit Scores?

Yes, there are multiple types of credit scores, each calculated using different models and criteria. The most common types include:

- FICO Score: Created by the Fair Isaac Corporation, this score is widely used by lenders to assess credit risk.

- VantageScore: Developed by the three major credit bureaus, this score provides an alternative to the FICO score.

While each scoring model has its nuances, the fundamental principles remain consistent, focusing on the same key components. Understanding the differences between these scores can help you better navigate the credit landscape.

What Impacts Your Credit Score?

Your credit score is influenced by various factors, some of which are within your control, while others may be less so. Here's a look at what can impact your score:

- Payment Timeliness: Consistently making payments on time has a positive impact, while late payments can significantly lower your score.

- Credit Utilization: High credit card balances relative to your limit can negatively affect your score.

- Credit Mix: Having a diverse mix of credit accounts, such as credit cards, mortgages, and installment loans, can be beneficial.

- Credit Inquiries: Each hard inquiry, such as applying for a new credit card, can slightly reduce your score.

Understanding these factors helps you make informed decisions that positively influence your credit score.

Credit Scores and Loan Approval

Your credit score plays a pivotal role in determining your eligibility for loans, as lenders rely on it to assess your creditworthiness. Here's how it affects the loan approval process:

- Eligibility: A higher credit score increases your chances of being approved for loans, as it indicates a lower risk to lenders.

- Loan Terms: With a high credit score, you may qualify for lower interest rates and more favorable loan terms, resulting in significant savings over time.

- Loan Amount: Your credit score can also influence the maximum loan amount you're eligible to receive.

Maintaining a good credit score is essential for securing loans and accessing better financial opportunities.

Credit Scores and Credit Cards

Credit scores are crucial when it comes to obtaining credit cards. Here's how they impact your credit card options:

- Approval Odds: A higher credit score improves your chances of being approved for credit cards, especially those with attractive rewards and benefits.

- Credit Limits: Your credit score can affect the credit limit you're offered, with higher scores typically resulting in higher limits.

- Interest Rates: A good credit score can qualify you for lower interest rates on credit cards, reducing the cost of carrying a balance.

Understanding the relationship between credit scores and credit cards can help you make informed decisions and maximize your credit card benefits.

How Do Credit Scores Affect Interest Rates?

Credit scores significantly impact the interest rates you're offered on loans and credit cards. Here's how it works:

- Risk Assessment: Lenders use your credit score to assess the risk of lending to you. A higher score indicates a lower risk, leading to more favorable interest rates.

- Cost Savings: Lower interest rates mean you pay less in interest over the life of a loan, resulting in significant cost savings.

- Loan Terms: Your credit score can also influence the terms of the loan, including the length and repayment schedule.

Maintaining a good credit score is crucial for securing loans with low interest rates and favorable terms.

The Importance of Monitoring Your Credit Score

Regularly monitoring your credit score is essential for maintaining financial health. Here's why it's important:

- Detecting Errors: Monitoring your score helps you identify errors or inaccuracies on your credit report, allowing you to address them promptly.

- Tracking Progress: Keeping an eye on your credit score enables you to track your progress as you work towards improving your financial standing.

- Preventing Identity Theft: Regular monitoring can help you detect signs of identity theft early, allowing you to take action to protect your personal information.

Utilizing credit monitoring services or regularly checking your credit report can help you stay informed and proactive about your credit health.

Common Myths About Credit Scores

There are several misconceptions about credit scores that can lead to confusion. Here are some common myths debunked:

- Myth #1: Checking Your Credit Score Lowers It: Checking your own credit score through a soft inquiry does not affect your score. Only hard inquiries, such as applying for a loan, can have a minor impact.

- Myth #2: Closing Old Accounts Can Improve Your Score: Closing old credit accounts can actually lower your score by reducing your credit history length and increasing your credit utilization ratio.

- Myth #3: Paying Off Debt Immediately Boosts Your Score: While paying off debt is beneficial, it may not immediately improve your score, as it depends on other factors like credit utilization and payment history.

Understanding the truth behind these myths can help you make informed decisions that positively impact your credit score.

FAQs About Credit Scores

Here are some frequently asked questions about credit scores, along with their answers:

- What is considered a good credit score? A good credit score typically falls between 670 and 739, while scores above 740 are considered excellent.

- How often should I check my credit score? It's a good idea to check your credit score at least once a year or before making significant financial decisions.

- Can I improve my credit score quickly? While improving your score takes time, making timely payments and reducing credit card balances can help boost it over time.

- Do utility bills affect my credit score? Generally, utility bills don't directly impact your score unless they're reported to credit bureaus for late payments.

- How long do negative items stay on my credit report? Negative items, like late payments and defaults, can stay on your credit report for up to seven years.

- Is it possible to have no credit score? Yes, if you have little to no credit history, you may not have a credit score.

Conclusion

In conclusion, a credit score is a vital component of your financial life, impacting everything from loan approvals to interest rates and credit card options. By understanding what a credit score is and how it's calculated, you can take proactive steps to improve and maintain a healthy score. Regularly monitoring your credit score, paying bills on time, and managing your credit utilization are essential practices for achieving financial stability. Stay informed, take control, and watch your credit score work in your favor.

You Might Also Like

Optimized Guide To Choosing The Perfect Fit: Size Shoe 8in Long FootRevitalize Your Routine: The Essential Guide To Good Mornings Workout

Chain Saws: Everything You Need To Know For Safe And Efficient Use

Squaring Numbers: Doubling And Understanding The Factor Of Increase

The Impact Of Schools Favouring Alumni In Hiring: A Comprehensive Analysis

Article Recommendations

- Meet The Talented Actor Behind Joe Goldberg Exploring The Stars Career And Role

- The Ultimate Guide To 80s Fashion Unleash Your Inner Icon

- Tom Welling Young A Stars Early Days And Rise To Fame