In today's fast-paced world, managing finances can be a daunting task. Whether you're an individual striving to pay off debts, a business aiming to streamline cash flow, or a student juggling tuition fees, a well-structured payment plan can be a lifesaver. It serves as a roadmap, guiding you through financial obligations and helping you achieve your goals without overwhelming stress. By breaking down large payments into manageable chunks, a payment plan can provide the clarity and confidence needed to navigate financial challenges.

Moreover, a payment plan is not just about organizing payments; it's about creating a strategic approach to financial management. It involves understanding your income, expenses, and financial commitments, and designing a plan that aligns with your unique situation. By doing so, you can avoid the pitfalls of late fees, interest charges, and financial uncertainty. Whether you're dealing with personal loans, credit card debt, or business expenses, a payment plan can be tailored to fit your needs, making it an invaluable tool for financial success.

Creating an effective payment plan requires careful consideration and planning. It's not a one-size-fits-all solution, and it's crucial to customize it to your specific circumstances. With the right approach, a payment plan can empower you to take control of your finances, reduce stress, and ultimately, achieve your financial objectives. In this comprehensive guide, we'll explore the strategies, benefits, and steps involved in crafting a payment plan that works for you.

Table of Contents

- What is a Payment Plan?

- Why Should You Use a Payment Plan?

- Benefits of Implementing a Payment Plan

- How to Create a Payment Plan?

- Payment Plans for Individuals

- Payment Plans for Businesses

- Payment Plans for Students

- Common Mistakes to Avoid in Payment Plans

- Tools and Resources for Managing Payment Plans

- Legal Aspects of Payment Plans

- How to Negotiate a Payment Plan?

- The Role of Technology in Payment Plans

- Understanding Flexibility in Payment Plans

- Examples of Successful Payment Plans

- Frequently Asked Questions

- Conclusion

What is a Payment Plan?

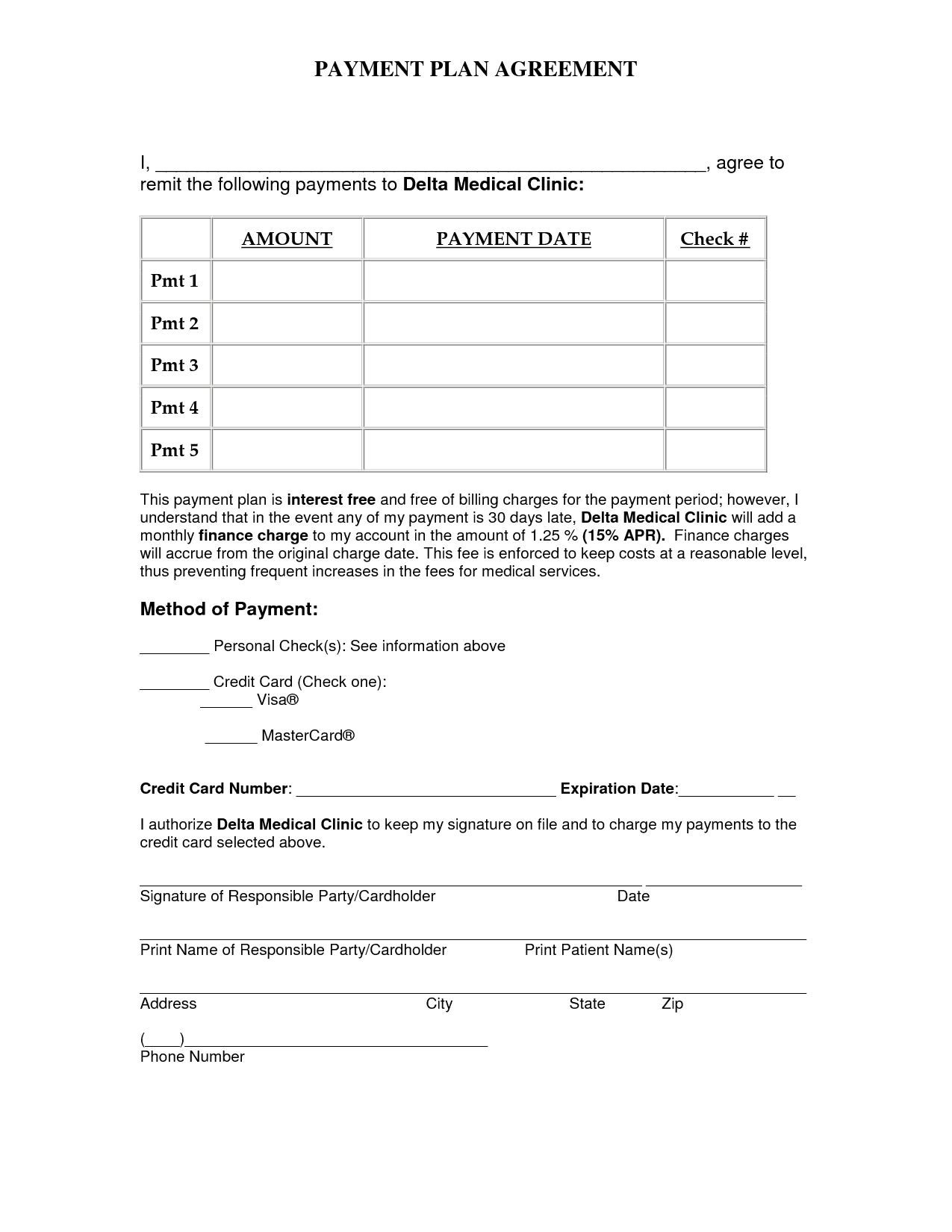

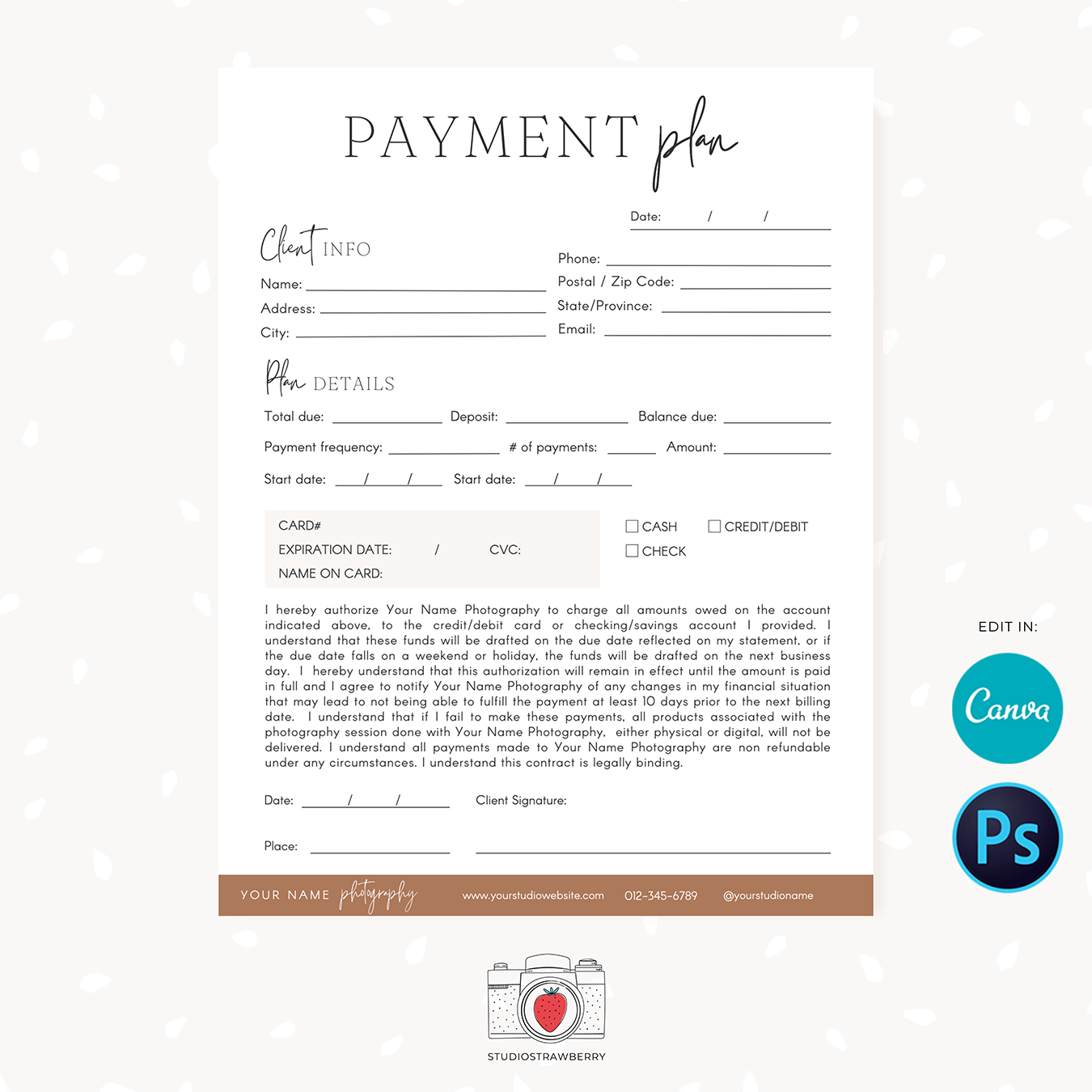

A payment plan is a structured schedule that outlines how an individual or business will pay off a debt or financial obligation over a specific period. It breaks down the total amount owed into smaller, more manageable payments, which are typically made on a regular basis, such as weekly, bi-weekly, or monthly. Payment plans are commonly used for loans, credit card debts, medical bills, and large purchases, providing a systematic approach to managing financial commitments.

In essence, a payment plan serves as a financial roadmap, helping individuals and businesses manage their finances more effectively. It allows for better budgeting and financial planning, ensuring that payments are made on time and in full. By adhering to a payment plan, one can avoid the consequences of missed payments, such as late fees, interest charges, and negative impacts on credit scores.

Depending on the nature of the debt or obligation, payment plans can be customized to suit the specific needs and circumstances of the payer. For instance, a payment plan for a student loan might differ significantly from that of a mortgage payment plan. The key is to tailor the plan to align with the payer's financial situation, ensuring affordability and sustainability over the duration of the plan.

Why Should You Use a Payment Plan?

There are several compelling reasons to consider using a payment plan, whether you're an individual, a business, or a student. Here are some of the primary benefits:

- Budgeting Made Easier: A payment plan helps you organize your finances by breaking down a large financial commitment into smaller, predictable payments. This makes it easier to budget and allocate funds accordingly.

- Reduced Financial Stress: Knowing exactly how much you need to pay and when can significantly reduce financial stress. A payment plan provides clarity and peace of mind, allowing you to focus on other important aspects of your life.

- Avoiding Late Fees and Penalties: By sticking to a payment plan, you can avoid the costly consequences of missed or late payments, such as late fees and interest charges.

- Improved Credit Score: Consistently making payments on time can positively impact your credit score, making it easier to secure loans and credit in the future.

- Flexibility: Payment plans can be tailored to fit your specific financial situation, providing flexibility and adaptability as your circumstances change.

Overall, a payment plan can be an invaluable tool for managing your finances, ensuring that you stay on track and meet your financial obligations without unnecessary stress or hardship.

Benefits of Implementing a Payment Plan

Implementing a payment plan offers numerous advantages, both in the short term and long term. Here are some key benefits to consider:

- Financial Discipline: A payment plan encourages financial discipline by requiring you to adhere to a structured payment schedule. This can help you develop better money management habits over time.

- Predictability: Knowing what you owe and when you owe it provides predictability in your financial life, making it easier to plan for future expenses and investments.

- Debt Reduction: By consistently making payments, you can gradually reduce your debt over time, ultimately achieving financial freedom.

- Peace of Mind: A well-structured payment plan can alleviate financial anxiety, allowing you to focus on other important aspects of your life without being burdened by financial worries.

- Improved Financial Relationships: Adhering to a payment plan can enhance your relationships with creditors, lenders, and service providers, as it demonstrates your commitment to meeting your financial obligations.

Overall, implementing a payment plan can lead to improved financial well-being, greater stability, and a more secure financial future.

How to Create a Payment Plan?

Creating a payment plan involves a series of steps to ensure that it's effective and tailored to your unique financial situation. Here's a step-by-step guide to help you get started:

- Assess Your Financial Situation: Begin by taking stock of your income, expenses, and debts. This will give you a clear picture of your financial standing and help you determine how much you can afford to pay each month.

- Identify Your Financial Goals: Determine what you want to achieve with your payment plan. Whether it's paying off a specific debt, saving for a future expense, or managing cash flow, having clear goals will guide your plan.

- Calculate Your Payments: Based on your financial assessment and goals, calculate how much you can afford to pay each period. Be realistic and ensure that the payments are manageable within your budget.

- Negotiate Terms: If you're working with a creditor or service provider, negotiate the terms of your payment plan to ensure they align with your financial capabilities. Be transparent about your situation and seek a mutually beneficial agreement.

- Create a Schedule: Establish a payment schedule that outlines when each payment is due. This could be weekly, bi-weekly, or monthly, depending on your financial situation and agreement with the creditor.

- Monitor and Adjust: Regularly monitor your progress and make adjustments as needed. If your financial situation changes, be proactive in revising your payment plan to ensure it remains effective and sustainable.

By following these steps, you can create a payment plan that works for you, helping you manage your finances more effectively and achieve your financial goals.

Payment Plans for Individuals

For individuals, payment plans can be an essential tool for managing personal finances, especially when dealing with debts, loans, and large expenses. Here are some common types of payment plans for individuals:

- Debt Repayment Plans: These plans are designed to help individuals pay off debts, such as credit card balances, personal loans, and medical bills, over time. They typically involve making regular, fixed payments until the debt is fully paid off.

- Installment Plans: Installment plans are used for large purchases, such as appliances, electronics, or vehicles, allowing individuals to pay off the cost over a set period with regular payments.

- Student Loan Payment Plans: These plans help individuals manage student loan debt by breaking down payments into manageable amounts. Options include standard, income-driven, and extended repayment plans.

- Mortgage Payment Plans: For homeowners, mortgage payment plans outline the terms for repaying a home loan, typically over 15 to 30 years. These plans include fixed or adjustable interest rates and may offer options for refinancing or modification.

By utilizing payment plans, individuals can take control of their finances, reduce debt, and achieve their financial objectives in a structured and manageable way.

Payment Plans for Businesses

For businesses, payment plans play a crucial role in managing cash flow, maintaining healthy financial relationships, and ensuring operational stability. Here are some common types of payment plans for businesses:

- Supplier Payment Plans: Businesses often negotiate payment terms with suppliers to spread out the cost of inventory, materials, or services over time, improving cash flow and liquidity.

- Customer Payment Plans: Offering payment plans to customers can increase sales and customer satisfaction by making products or services more affordable through installment payments.

- Lease Payment Plans: Businesses that lease equipment, vehicles, or property typically have structured payment plans that outline the terms and schedule for lease payments.

- Loan Repayment Plans: Businesses with loans or lines of credit can use payment plans to manage debt repayment, ensuring that payments are made on time and in accordance with loan agreements.

By implementing payment plans, businesses can effectively manage their financial commitments, optimize cash flow, and build strong relationships with suppliers, customers, and financial institutions.

Payment Plans for Students

For students, managing tuition fees and educational expenses can be challenging. Payment plans provide a practical solution for spreading out these costs over time. Here are some common payment plans for students:

- Tuition Payment Plans: Many educational institutions offer tuition payment plans that allow students to pay their tuition fees in installments rather than in a lump sum. This can ease the financial burden and make education more accessible.

- Student Loan Repayment Plans: After graduation, students often face the challenge of repaying student loans. Various repayment plans are available, including standard, income-driven, and graduated plans, to accommodate different financial situations.

- Textbook and Supply Payment Plans: Some colleges and universities offer payment plans for textbooks and supplies, spreading the cost over the academic term or year.

By utilizing payment plans, students can manage their educational expenses more effectively, reducing financial stress and focusing on their studies.

Common Mistakes to Avoid in Payment Plans

While payment plans can be highly beneficial, there are common mistakes that individuals and businesses should avoid to ensure their effectiveness:

- Unrealistic Payment Amounts: Setting payments that are too high for your budget can lead to missed payments and financial strain. Be realistic about what you can afford.

- Ignoring Changes in Financial Situation: Failing to adjust the payment plan when your financial situation changes can lead to difficulties in meeting payments. Be proactive in revising your plan as needed.

- Overlooking Fees and Penalties: Some payment plans may include fees or penalties for missed or late payments. Be aware of these terms and strive to meet payment deadlines.

- Lack of Communication: If you're struggling with payments, communicate with creditors or service providers to negotiate terms or find alternative solutions. Ignoring the issue can worsen the situation.

By avoiding these common mistakes, you can ensure that your payment plan remains effective and supports your financial goals.

Tools and Resources for Managing Payment Plans

There are various tools and resources available to help individuals and businesses manage payment plans effectively. Here are some useful options:

- Budgeting Apps: Apps like Mint, YNAB (You Need a Budget), and Personal Capital can help you track your finances, set budgets, and manage payment schedules.

- Financial Advisors: Consulting with a financial advisor can provide personalized guidance and strategies for creating and managing payment plans.

- Online Calculators: Online payment calculators can help you estimate monthly payments and interest costs for loans, mortgages, and other debts.

- Educational Resources: Websites, books, and courses on personal finance and debt management can provide valuable insights and tips for managing payment plans effectively.

By leveraging these tools and resources, you can enhance your ability to manage payments, achieve financial stability, and reach your financial goals.

Legal Aspects of Payment Plans

Understanding the legal aspects of payment plans is important to ensure compliance and protect your rights as a payer. Here are some key considerations:

- Contractual Agreements: Payment plans often involve contractual agreements that outline the terms and conditions of the plan. It's essential to read and understand these terms before agreeing to a plan.

- Consumer Protection Laws: Be aware of consumer protection laws that may apply to your payment plan, such as laws governing credit, debt collection, and financial agreements.

- Dispute Resolution: If you encounter issues with a payment plan, understand the process for resolving disputes, which may involve negotiation, mediation, or legal action.

By understanding the legal aspects of payment plans, you can ensure that your rights are protected and that you comply with applicable laws and regulations.

How to Negotiate a Payment Plan?

Negotiating a payment plan can be a crucial step in ensuring that it aligns with your financial capabilities. Here are some tips for successful negotiation:

- Be Transparent: Clearly communicate your financial situation and limitations to the creditor or service provider. Honesty can lead to more favorable terms.

- Know Your Options: Research different payment plan options and understand what terms are reasonable before entering negotiations.

- Seek Flexibility: Request flexibility in payment terms, such as adjusting due dates or payment amounts, to accommodate your financial situation.

- Document Agreements: Once terms are agreed upon, ensure that all agreements are documented in writing to avoid misunderstandings or disputes later on.

By negotiating effectively, you can create a payment plan that is manageable and sustainable, helping you meet your financial obligations with confidence.

The Role of Technology in Payment Plans

Technology plays a significant role in enhancing the management and execution of payment plans. Here are some ways technology contributes to payment plans:

- Automation: Automated payment systems can streamline the payment process, reducing the risk of missed payments and ensuring timely transactions.

- Online Platforms: Online platforms and portals allow individuals and businesses to manage payment plans digitally, providing access to payment history, schedules, and account information.

- Mobile Apps: Mobile apps offer convenience and accessibility, enabling users to monitor and manage payments on the go.

- Data Analysis: Technology can provide valuable insights through data analysis, helping users optimize payment plans and identify opportunities for savings.

By leveraging technology, individuals and businesses can improve the efficiency and effectiveness of their payment plans, ultimately achieving better financial outcomes.

Understanding Flexibility in Payment Plans

Flexibility is a key component of successful payment plans, allowing individuals and businesses to adapt to changing financial circumstances. Here's how flexibility can be achieved:

- Adjustable Payment Amounts: Some payment plans allow for adjustments in payment amounts based on income fluctuations or financial changes.

- Variable Payment Schedules: Payment schedules can be modified to accommodate changes in cash flow, such as shifting from monthly to bi-monthly payments.

- Early Payment Options: Many payment plans offer the option to make early payments without penalties, allowing for faster debt reduction.

By incorporating flexibility into payment plans, individuals and businesses can ensure that they remain manageable and sustainable, even in the face of financial challenges.

Examples of Successful Payment Plans

Examining successful payment plans can provide valuable insights and inspiration for creating your own. Here are a few examples:

- Debt Snowball Method: This payment plan involves paying off smaller debts first while making minimum payments on larger debts. As smaller debts are eliminated, payments are rolled into larger debts, accelerating the payoff process.

- Business Installment Agreements: A business negotiated a payment plan with a supplier, spreading out the cost of inventory over several months. This improved cash flow and allowed for continued operations without financial strain.

- Flexible Tuition Payment Plans: A university offered students a flexible payment plan, allowing them to adjust payment amounts based on income changes. This increased enrollment and reduced financial stress for students.

By learning from successful payment plans, you can apply similar strategies to your own financial situation, enhancing your chances of success.

Frequently Asked Questions

1. What are the key elements of a successful payment plan?

A successful payment plan should include realistic payment amounts, a clear schedule, flexibility to adapt to changes, and open communication with creditors or service providers.

2. Can I negotiate a payment plan with my creditors?

Yes, negotiating a payment plan with creditors is possible and often advisable. Being transparent about your financial situation can lead to more favorable terms.

3. How can I ensure that I stick to my payment plan?

To stick to your payment plan, set up automated payments, regularly review your financial situation, and communicate with creditors if you encounter difficulties.

4. Are there any legal protections for payment plans?

Yes, consumer protection laws may apply to payment plans, ensuring that terms are fair and that debt collection practices are lawful. Understanding these laws can protect your rights.

5. What should I do if I can't afford my payment plan?

If you can't afford your payment plan, contact your creditor or service provider to discuss options, such as adjusting payment amounts or seeking temporary relief.

6. How does a payment plan affect my credit score?

Sticking to a payment plan and making payments on time can positively impact your credit score, while missed payments can have a negative effect. It's important to adhere to the agreed-upon schedule.

Conclusion

In conclusion, a well-structured payment plan is an invaluable tool for managing finances, whether for individuals, businesses, or students. By understanding the key components, benefits, and strategies for effective payment plans, you can take control of your financial future and achieve your goals with confidence. Remember to stay flexible, communicate openly with creditors, and leverage available tools and resources to optimize your payment plan. With a thoughtful approach, you can navigate financial challenges successfully and enjoy greater financial stability and peace of mind.

You Might Also Like

Mastering The Forearm Curls: A Guide To Building Strength And EnduranceMastering The Uber Driver App: Your Ultimate Guide To Success

Bay Leaf Leaves: The Aromatic Marvel Of Culinary And Medicinal World

Maximize Your Earnings: UPS Driver Salary Insights For 2023

All You Need To Know About Ninja Motorcycle: Features, Performance, And More

Article Recommendations

- Exploring The World Of Mkvmoviespoint Everything You Need To Know

- The Ultimate Guide To 80s Fashion Unleash Your Inner Icon

- The Life And Family Of Niall Horan An Indepth Look At His Wife And Son