In today's fast-paced financial world, having a good credit score is more important than ever. Whether you're planning to buy a home, finance a car, or simply qualify for a new credit card, understanding how to raise your credit score can have a profound impact on your financial health. Many people overlook the importance of maintaining a solid credit score, but it can be a crucial factor in securing favorable loan terms and interest rates. It's essential to be proactive in managing your credit score to ensure you're in the best possible position for future financial opportunities.

Credit scores are calculated based on several factors, including payment history, credit utilization, length of credit history, and more. Each of these components plays a vital role in determining your overall creditworthiness. By familiarizing yourself with the elements that affect your score, you can take strategic steps to improve it. The process may seem daunting at first, but with the right guidance and a bit of effort, you can see significant improvements over time.

In this comprehensive guide, we'll explore various methods to boost your credit score effectively. From understanding the basics of credit scoring to implementing practical tips, this article aims to provide you with the knowledge and tools needed to enhance your financial standing. By following these strategies, you'll be well on your way to achieving a higher credit score and unlocking more financial opportunities. Let's dive in and discover how you can take control of your credit score today.

Table of Contents

- Understanding Credit Scores

- Why Are Credit Scores Important?

- Key Factors Affecting Your Credit Score

- How Does Payment History Impact Your Score?

- What is Credit Utilization and Why is it Significant?

- Length of Credit History

- How Do New Credit Accounts Affect Your Score?

- Types of Credit Used

- Effective Strategies to Raise Your Credit Score

- Monitoring Your Credit Report Regularly

- How to Dispute Inaccuracies on Your Credit Report?

- Building Credit from Scratch

- Rebuilding Damaged Credit

- Frequently Asked Questions

- Conclusion

Understanding Credit Scores

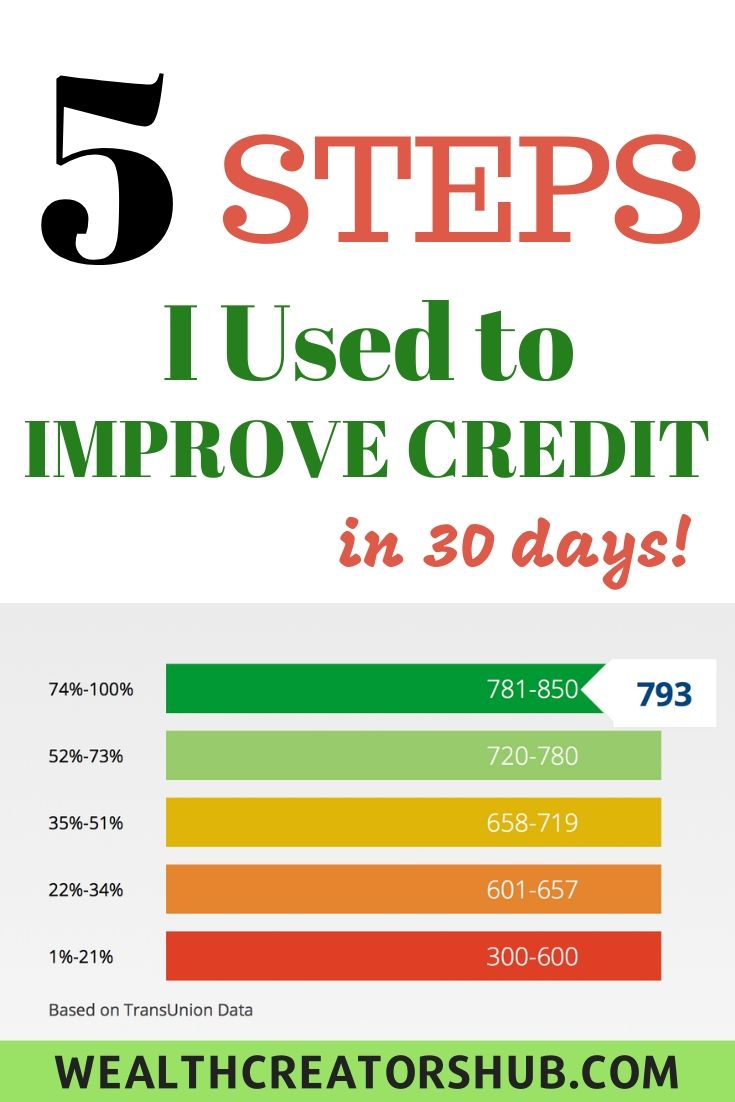

Credit scores are numerical representations of a person's creditworthiness, used by lenders to evaluate the likelihood of repayment. These scores, typically ranging from 300 to 850, are developed by credit bureaus like Experian, Equifax, and TransUnion. The higher the score, the better the creditworthiness.

Several scoring models exist, with FICO and VantageScore being the most commonly used. Each model has its own criteria and weightings but generally considers similar factors such as payment history, credit utilization, and more.

Understanding how these scores are calculated can empower consumers to make informed financial decisions. By knowing what affects your credit score, you can take targeted actions to improve it, ultimately leading to better loan terms and interest rates.

Why Are Credit Scores Important?

Credit scores play a crucial role in the financial world, impacting everything from loan approvals to interest rates. A higher credit score can lead to favorable loan terms, saving you money in the long run. Conversely, a lower score may result in higher interest rates and even loan denials.

Beyond loans, credit scores can affect various aspects of your financial life, including renting an apartment, securing a job, and even setting insurance premiums. Landlords, employers, and insurers may use your credit score as part of their decision-making process.

Maintaining a good credit score is essential for financial stability and can open doors to numerous opportunities. By prioritizing your credit score, you can ensure access to the best financial products and services available.

Key Factors Affecting Your Credit Score

Several key factors contribute to your credit score, each carrying different weightings:

- Payment History: Accounts for 35% of your score, emphasizing the importance of on-time payments.

- Credit Utilization: Makes up 30% of your score, highlighting the need to keep balances low relative to credit limits.

- Length of Credit History: Constitutes 15% of your score, reflecting the benefit of a long credit history.

- New Credit: Comprises 10% of your score, considering recent credit inquiries and new accounts.

- Credit Mix: Also accounts for 10% of your score, rewarding a diverse range of credit types.

By understanding these factors, you can focus on the areas that need improvement and work towards a higher credit score.

How Does Payment History Impact Your Score?

Payment history is the most significant factor in determining your credit score, as it accounts for 35% of the total calculation. It reflects your track record of repaying debts, including credit cards, loans, and other financial obligations.

Consistently making on-time payments demonstrates reliability and financial responsibility, leading to a higher credit score. Conversely, late payments, defaults, and bankruptcies can significantly damage your score.

To improve your payment history:

- Set up automatic payments or reminders to ensure timely payments.

- Prioritize paying off high-interest debts first.

- Communicate with creditors if you're unable to make a payment, as they may offer alternative arrangements.

By maintaining a positive payment history, you'll be well on your way to a higher credit score.

What is Credit Utilization and Why is it Significant?

Credit utilization refers to the percentage of your available credit that you're currently using. It is the second most important factor in your credit score calculation, accounting for 30% of the total score.

To calculate your credit utilization ratio, divide your total credit card balances by your total credit limits, then multiply by 100 to get a percentage. A lower credit utilization ratio indicates responsible credit usage and positively impacts your score.

To maintain a healthy credit utilization ratio:

- Keep balances below 30% of your credit limit.

- Pay off credit card balances in full each month if possible.

- Consider requesting a credit limit increase to reduce your utilization ratio.

By managing your credit utilization effectively, you can enhance your credit score and demonstrate financial responsibility.

Length of Credit History

The length of your credit history contributes 15% to your overall credit score. This factor considers the age of your oldest account, the age of your newest account, and the average age of all your accounts.

A longer credit history is generally viewed more favorably, as it provides more data on your financial behavior over time. However, even individuals with a shorter credit history can achieve a good score by responsibly managing their debts.

To optimize the length of your credit history:

- Avoid closing old credit accounts, as they contribute to the overall age of your credit.

- Be cautious when opening new accounts, as they can lower your average account age.

By maintaining a long and positive credit history, you can enhance your score and demonstrate creditworthiness to lenders.

How Do New Credit Accounts Affect Your Score?

New credit accounts and inquiries contribute 10% to your credit score. Opening several new accounts within a short period can signal financial instability to lenders and negatively impact your score.

Each time you apply for new credit, a hard inquiry is added to your credit report. Too many hard inquiries within a short timeframe can lower your score, as they indicate a potential increase in financial risk.

To manage new credit accounts effectively:

- Limit the number of new credit applications within a short period.

- Consider spacing out new credit applications to minimize the impact on your score.

- Focus on building a solid credit history with existing accounts before seeking additional credit.

By handling new credit accounts wisely, you can protect your credit score and maintain financial stability.

Types of Credit Used

Types of credit used, contributing 10% to your score, refer to the variety of credit accounts you have, such as credit cards, mortgages, auto loans, and personal loans. A diverse credit mix can positively influence your score, as it demonstrates your ability to manage different types of credit responsibly.

However, it's essential to remember that the impact of credit mix is relatively minor compared to other factors. It should be considered in conjunction with other aspects of your credit profile.

To optimize your credit mix:

- Maintain a balance of revolving and installment credit accounts.

- Avoid opening unnecessary accounts just to diversify your credit mix.

By effectively managing different types of credit, you can enhance your credit score and illustrate your financial responsibility.

Effective Strategies to Raise Your Credit Score

Improving your credit score requires a strategic approach, focusing on the areas that have the most significant impact. Here are some effective strategies to consider:

- Pay Bills on Time: Consistently making payments on time is crucial for a high credit score.

- Reduce Debt: Lowering your outstanding balances can improve your credit utilization ratio.

- Avoid New Hard Inquiries: Limiting new credit applications can prevent unnecessary score reductions.

- Monitor Your Credit Report: Regularly checking your credit report can help you identify and correct errors.

- Increase Credit Limits: Requesting a credit limit increase can lower your credit utilization ratio.

By implementing these strategies, you can make significant progress in raising your credit score and improving your financial standing.

Monitoring Your Credit Report Regularly

Regular monitoring of your credit report is an essential part of maintaining a healthy credit score. By reviewing your report, you can identify errors, detect potential fraudulent activity, and track your progress over time.

Each of the major credit bureaus—Experian, Equifax, and TransUnion—offers a free annual credit report. It's advisable to check your report from each bureau to ensure accuracy and consistency.

When reviewing your credit report, pay attention to the following:

- Personal Information: Ensure your name, address, and social security number are accurate.

- Account Information: Verify the accuracy of your account balances, credit limits, and payment history.

- Inquiries: Check for unauthorized credit inquiries that could indicate identity theft.

By staying vigilant and monitoring your credit report regularly, you can protect your credit score and financial well-being.

How to Dispute Inaccuracies on Your Credit Report?

If you identify inaccuracies on your credit report, it's crucial to address them promptly. Disputing errors can help improve your credit score and ensure that your credit profile accurately reflects your financial behavior.

Here's a step-by-step guide to disputing inaccuracies:

- Gather Evidence: Collect any supporting documents that demonstrate the error, such as account statements or payment receipts.

- Contact the Credit Bureau: Submit a dispute through the credit bureau's online platform, by mail, or by phone.

- Provide Detailed Information: Clearly explain the error and include copies of supporting documents.

- Follow Up: Monitor the progress of your dispute and follow up if necessary. The credit bureau is required to investigate within 30 days.

- Check Your Report: Once the dispute is resolved, verify that the correction has been made on your credit report.

By taking action to dispute inaccuracies, you can improve your credit score and ensure a fair representation of your financial history.

Building Credit from Scratch

For individuals without a credit history, building credit from scratch can be a challenging but rewarding process. Establishing a credit history is essential for accessing financial products and achieving a high credit score.

Here are some steps to start building credit:

- Open a Secured Credit Card: Secured credit cards require a deposit and are an excellent way to establish credit.

- Become an Authorized User: Ask a family member to add you as an authorized user on their credit card.

- Take Out a Credit-Builder Loan: These loans are specifically designed for individuals looking to build credit.

- Pay Bills on Time: Consistently making on-time payments is crucial for establishing a positive credit history.

By taking these steps, you can lay the foundation for a strong credit profile and work toward achieving a high credit score.

Rebuilding Damaged Credit

Rebuilding damaged credit can be a challenging process, but it's possible with dedication and the right strategies. Whether you've experienced bankruptcy, foreclosure, or other financial setbacks, improving your credit score is achievable.

Here are some tips for rebuilding damaged credit:

- Create a Budget: Develop a budget to manage expenses and prioritize debt repayment.

- Set Up Payment Plans: Work with creditors to establish manageable payment plans.

- Focus on Secured Credit: Use secured credit cards or loans to rebuild credit responsibly.

- Monitor Progress: Regularly check your credit report to track improvements and identify areas for further action.

With patience and persistence, you can rebuild your credit and achieve a healthier financial future.

Frequently Asked Questions

1. What is a good credit score?

A good credit score typically ranges from 670 to 739, depending on the scoring model. Scores above 740 are considered very good, while scores above 800 are considered excellent.

2. How often should I check my credit score?

It's advisable to check your credit score at least once a year. However, monitoring it more frequently can help you stay informed about any changes or potential issues.

3. Can I improve my credit score quickly?

Improving your credit score takes time and consistent effort. While there are no quick fixes, focusing on paying bills on time and reducing debt can lead to gradual improvements.

4. How long do negative items stay on my credit report?

Negative items, such as late payments or foreclosures, can remain on your credit report for up to seven years. Bankruptcies can stay for up to 10 years.

5. Does checking my credit score lower it?

No, checking your own credit score is considered a soft inquiry and does not affect your score. Only hard inquiries, such as applying for new credit, can impact your score.

6. Can I raise my credit score by closing old accounts?

Closing old accounts can actually lower your credit score by reducing your credit history length and increasing your credit utilization ratio. It's generally advisable to keep old accounts open.

Conclusion

Raising your credit score is a vital step towards achieving financial stability and accessing favorable credit terms. By understanding the factors that influence your score and implementing effective strategies, you can work towards a healthier credit profile. Whether you're building credit from scratch or recovering from financial setbacks, maintaining a proactive approach and staying informed are key to success. With dedication and perseverance, you can raise your credit score and unlock a world of financial opportunities.

For additional resources and guidance on improving your credit score, consider visiting reputable financial education websites such as the Consumer Financial Protection Bureau.

You Might Also Like

Greek Mythology Movies: A Cinematic OdysseyThe Mystique Of Secret Societies: Hidden Dimensions And Influence

Unraveling The Impact Of "The Dark Knight Returns": A Comprehensive Insight

Understanding The Dynamics Of Sex AI Chat: A Comprehensive Guide To The Future Of Intimacy

Chat GPT: The Power Of AI Language Models

Article Recommendations

- One Direction Liam Payne Zayn Malik A Look Back

- Exploring The World Of Mkvmoviespoint Everything You Need To Know

- Shirley Jones A Timeless Icon Of Film And Television

![7 Tips to Increase Your Credit Score [Infographic]](http://www.trimurty.com/blog/wp-content/uploads/2016/12/Infographic-7-01-1.jpg)