When it comes to purchasing a home, one of the most critical factors to consider is the average home interest rate. It plays a significant role in determining the affordability of a mortgage and the overall cost of homeownership. By understanding the average home interest rate, potential homeowners can make informed decisions about when to buy, how much to borrow, and what type of mortgage to choose. The average home interest rate is influenced by various factors, including the state of the economy, monetary policy, and individual creditworthiness. It's essential to stay informed about these rates, as they can fluctuate and impact your financial planning.

The average home interest rate is not a static figure; it can vary based on a range of economic indicators, lender policies, and individual borrower profiles. For instance, a robust economy might lead to higher rates as demand for loans increases, while a sluggish economy could prompt lower rates to stimulate borrowing. Additionally, central bank policies, such as those implemented by the Federal Reserve, can directly influence interest rates by adjusting the federal funds rate. For homebuyers, understanding these dynamics is crucial as they can significantly affect monthly mortgage payments and the total interest paid over the life of a loan.

Prospective homeowners should also be aware that the average home interest rate can differ based on the type of mortgage chosen, such as fixed-rate or adjustable-rate mortgages. Fixed-rate mortgages offer stability with a constant interest rate throughout the loan term, while adjustable-rate mortgages may start with lower rates that can change over time, potentially leading to higher payments. By considering these factors and staying updated on current rates, homebuyers can better navigate the real estate market, secure favorable loan terms, and ultimately achieve their homeownership goals.

Table of Contents

- Factors Influencing Interest Rates

- How Does the Economy Affect Interest Rates?

- The Role of Monetary Policy in Interest Rates

- Can Credit Scores Affect Your Interest Rate?

- Fixed vs. Adjustable Interest Rates: What's the Difference?

- Current Trends in the Average Home Interest Rate

- How to Compare Lender Rates Effectively?

- Is It Worth Locking in Your Interest Rate?

- How Interest Rates Impact Home Affordability?

- A Historical Perspective on Home Interest Rates

- International Comparison: Home Interest Rates Across the Globe

- Can We Predict Future Interest Rates?

- Expert Advice on Navigating Interest Rates

- Frequently Asked Questions

- Conclusion

Factors Influencing Interest Rates

Understanding the factors that influence the average home interest rate is crucial for potential homeowners and investors. Interest rates are determined by a combination of economic indicators, government policies, and market conditions. Key factors include:

- Economic Growth: When the economy is strong, with low unemployment and healthy GDP growth, interest rates tend to rise as demand for borrowing increases.

- Inflation: Higher inflation leads to higher interest rates as lenders demand more compensation for the decrease in purchasing power over time.

- Central Bank Policies: Central banks, such as the Federal Reserve, influence rates by setting the federal funds rate and through open market operations.

- Credit Market Conditions: The availability of credit and the risk appetite of lenders can also affect interest rates.

- Global Events: Geopolitical events and global economic trends can lead to changes in interest rates as markets react to uncertainty.

These factors collectively shape the landscape of the mortgage market and impact the cost of borrowing for homebuyers. Staying informed about these elements can help prospective homeowners make timely decisions regarding their mortgage.

How Does the Economy Affect Interest Rates?

The state of the economy plays a pivotal role in determining the average home interest rate. When the economy is robust, characterized by low unemployment and strong GDP growth, the demand for loans typically increases. This heightened demand can lead to higher interest rates as lenders capitalize on the opportunity to earn more from borrowers. Conversely, during economic downturns, interest rates may be lowered to encourage borrowing and stimulate economic activity.

Inflation is another economic factor that influences interest rates. When inflation is high, lenders require higher interest rates to compensate for the reduced purchasing power of future repayments. Central banks may also adjust rates to control inflation, impacting the cost of mortgages. For example, if inflation is rising, the Federal Reserve may increase the federal funds rate, which can lead to higher mortgage rates.

Moreover, the economic policies of the government, such as fiscal stimulus or tax changes, can indirectly affect interest rates by influencing economic growth and inflation. Understanding these economic dynamics can help borrowers anticipate changes in interest rates and plan their mortgage accordingly.

The Role of Monetary Policy in Interest Rates

Monetary policy is a critical tool used by central banks to manage the economy and control inflation. It directly influences the average home interest rate through mechanisms like the federal funds rate and open market operations. When central banks, such as the Federal Reserve, adjust the federal funds rate, it impacts the interest rates that banks charge each other for overnight loans. This, in turn, affects the rates banks offer to consumers for mortgages and other loans.

For instance, if the Federal Reserve lowers the federal funds rate, banks have access to cheaper capital, which can lead to lower mortgage rates for consumers. Conversely, when the federal funds rate is increased to curb inflation, mortgage rates are likely to rise as well. Central banks may also engage in open market operations, buying or selling government securities to influence the money supply and interest rates.

Understanding the role of monetary policy in shaping interest rates can help homebuyers anticipate changes and make informed decisions about the timing of their mortgage applications. Keeping an eye on central bank announcements and economic forecasts is a prudent strategy for anyone looking to purchase a home.

Can Credit Scores Affect Your Interest Rate?

Credit scores are a fundamental factor in determining the interest rate a borrower may qualify for when seeking a mortgage. A higher credit score typically translates to a lower interest rate, as it indicates to lenders that the borrower is a lower risk. Conversely, a lower credit score can lead to higher interest rates, increasing the cost of borrowing.

Lenders use credit scores to assess the likelihood of a borrower repaying the loan on time. A strong credit score reflects a history of timely payments, low credit utilization, and a mix of credit types. Borrowers with excellent credit scores may have access to the best rates available in the market, potentially saving thousands of dollars over the life of the loan.

It's essential for potential homebuyers to understand the impact of their credit score on the interest rates they may be offered. Improving one's credit score before applying for a mortgage can lead to more favorable loan terms and lower monthly payments. Steps such as paying down existing debt, avoiding new credit inquiries, and ensuring timely bill payments can enhance credit scores and improve borrowing conditions.

Fixed vs. Adjustable Interest Rates: What's the Difference?

When considering a mortgage, one of the key decisions is choosing between a fixed-rate and an adjustable-rate mortgage (ARM). Each option has its advantages and drawbacks, and understanding these differences is crucial for making an informed choice.

A fixed-rate mortgage offers stability and predictability, with the interest rate remaining constant throughout the life of the loan. This means that monthly payments are consistent, making budgeting easier for homeowners. Fixed-rate mortgages are ideal for those who plan to stay in their home for a long period and want to avoid the risk of rising rates.

On the other hand, an adjustable-rate mortgage typically starts with a lower interest rate than a fixed-rate mortgage. However, this rate is subject to change at specified intervals, which can result in fluctuating monthly payments. ARMs may be suitable for homebuyers who plan to sell or refinance before the rate adjustment period or for those expecting their income to increase.

Choosing between a fixed and adjustable interest rate depends on individual financial goals, risk tolerance, and the current interest rate environment. Prospective homeowners should carefully evaluate their options and consider consulting with a financial advisor to determine the best fit for their situation.

Current Trends in the Average Home Interest Rate

The average home interest rate is subject to constant change due to various economic and market factors. As of the latest data, interest rates have experienced fluctuations influenced by economic recovery efforts, inflation concerns, and central bank policies. Understanding these trends can help potential homebuyers make strategic decisions about when to enter the market.

In recent years, interest rates have been relatively low, driven by efforts to stimulate economic growth in the wake of global economic challenges. However, as economies recover and inflationary pressures mount, there is a possibility of interest rates rising in the near future. Homebuyers should monitor these trends and consider locking in rates if they anticipate increases.

Additionally, regional variations in interest rates may occur based on local economic conditions and housing market dynamics. Staying informed about both national and regional trends can provide a comprehensive understanding of the current interest rate landscape.

How to Compare Lender Rates Effectively?

Comparing lender rates is an essential step for homebuyers seeking the best mortgage deal. With numerous lenders offering various interest rates and loan terms, it's crucial to conduct thorough research and evaluate options to secure favorable conditions.

Here are some tips for effectively comparing lender rates:

- Shop Around: Contact multiple lenders to obtain rate quotes and compare their offers.

- Understand Terms: Pay attention to the terms and conditions associated with each lender's offers, including loan duration, fees, and prepayment penalties.

- Consider APR: The Annual Percentage Rate (APR) provides a comprehensive view of the cost of borrowing, including interest rates and fees.

- Evaluate Reputation: Research lender reviews and ratings to assess customer satisfaction and reliability.

- Seek Pre-Approval: Obtain pre-approval from multiple lenders to understand your borrowing capacity and interest rate eligibility.

By taking the time to compare lender rates, homebuyers can identify the most competitive offers and make informed decisions that align with their financial goals.

Is It Worth Locking in Your Interest Rate?

Locking in an interest rate is a decision that many homebuyers face during the mortgage process. A rate lock ensures that the interest rate agreed upon with the lender remains unchanged for a specified period, protecting the borrower from potential rate increases before closing the loan.

Rate locks can be beneficial in a rising interest rate environment, as they provide certainty and stability for borrowers. However, it's essential to consider the trade-offs, such as potential fees associated with extending the rate lock period if the loan closing is delayed.

Homebuyers should evaluate the current interest rate trends and consult with their lender to determine the appropriate timing and duration for a rate lock. While locking in a rate can offer peace of mind, it's crucial to assess the overall financial implications and ensure that the decision aligns with one's long-term homeownership goals.

How Interest Rates Impact Home Affordability?

Interest rates play a significant role in determining the affordability of a home. Even small changes in interest rates can have a substantial impact on monthly mortgage payments and the total cost of a loan over time.

When interest rates are low, borrowers can afford larger loan amounts, potentially expanding their options in the housing market. Conversely, higher interest rates may limit the size of the mortgage a borrower can qualify for, impacting the affordability of homes within certain price ranges.

To illustrate the impact of interest rates on affordability, consider a scenario where a 1% increase in the interest rate could add hundreds of dollars to monthly payments and thousands to the overall cost of the loan. Understanding these dynamics can help homebuyers make informed decisions about their budget and housing options.

Prospective homeowners should work closely with their lender to assess how interest rates affect their purchasing power and explore strategies for managing affordability, such as choosing different loan terms or considering adjustable-rate mortgages.

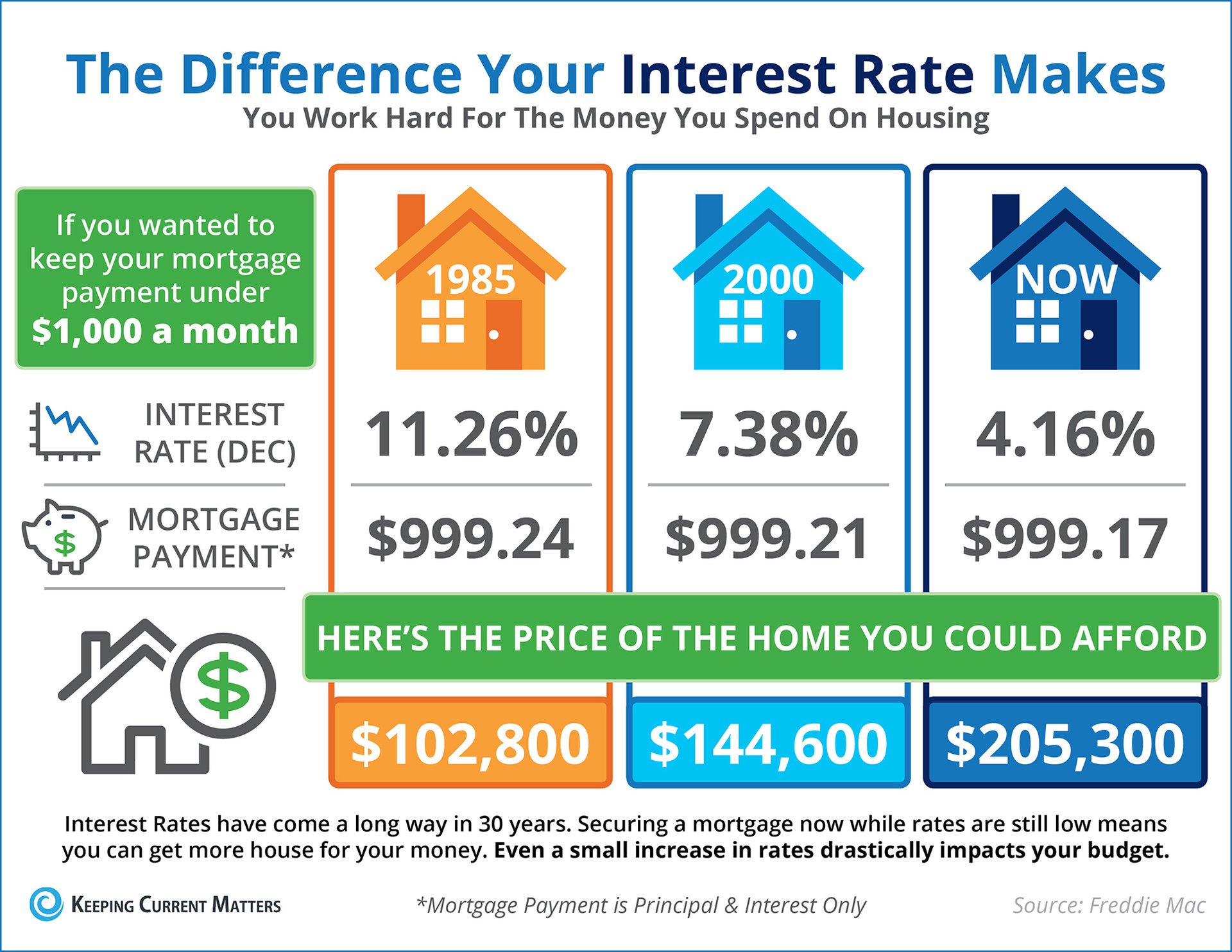

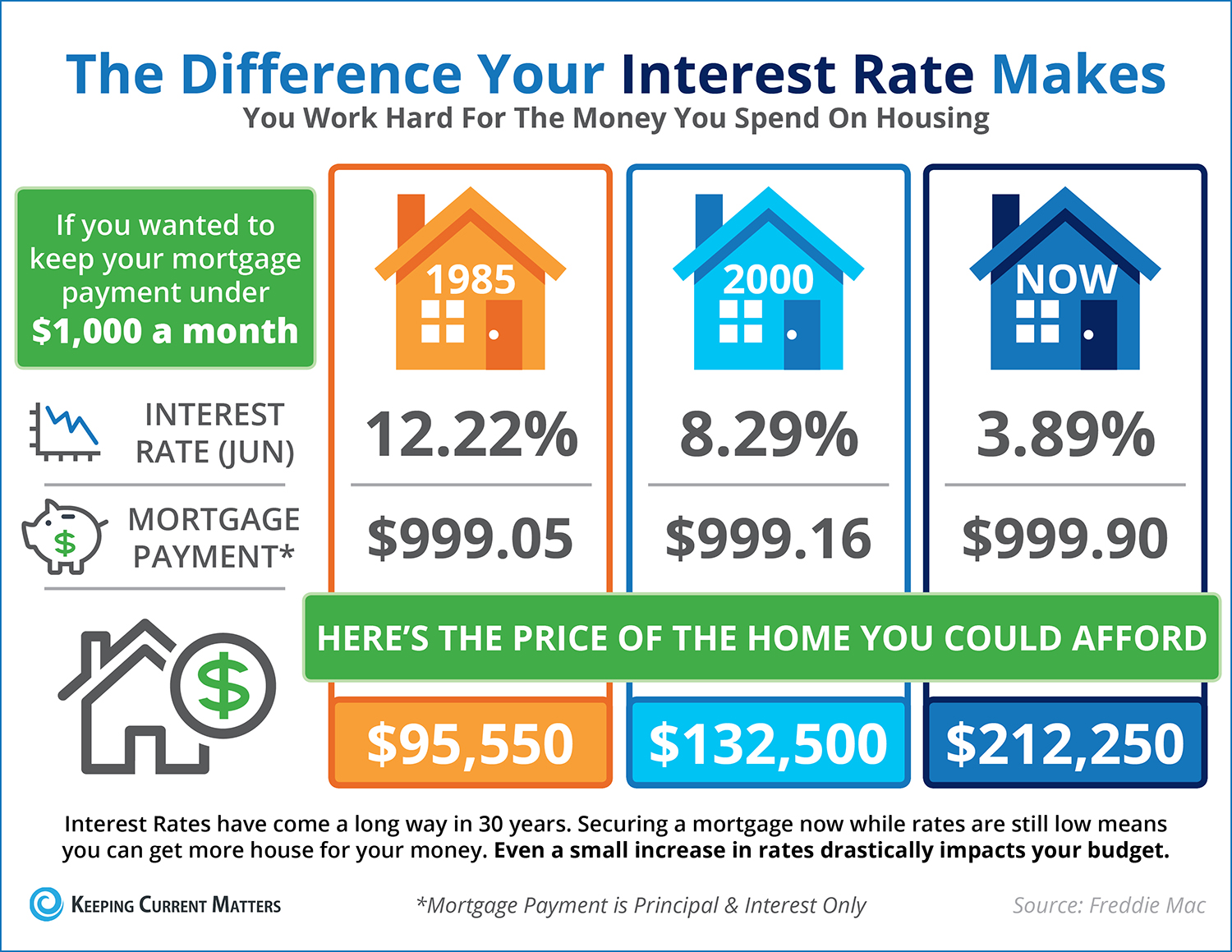

A Historical Perspective on Home Interest Rates

Examining historical trends in home interest rates provides valuable insights into the factors that have influenced borrowing costs over time. Understanding these patterns can help prospective homeowners anticipate future rate movements and make informed decisions.

Over the past several decades, home interest rates have experienced fluctuations due to various economic, political, and market conditions. In the 1980s, interest rates reached historically high levels as central banks sought to combat inflation. Since then, rates have generally trended downward, reaching record lows in the aftermath of the 2008 financial crisis and during recent economic challenges.

Studying these historical trends allows homebuyers to recognize the cyclical nature of interest rates and understand the potential for future changes. By staying informed about past and current rate environments, borrowers can make strategic decisions regarding the timing of their mortgage applications and the type of loan they choose.

International Comparison: Home Interest Rates Across the Globe

Interest rates vary significantly across different countries, influenced by each nation's economic conditions, central bank policies, and housing market dynamics. Comparing international home interest rates can provide valuable insights into global economic trends and offer context for domestic rate movements.

In some countries, interest rates may be lower due to strong economic performance and stable inflation, while others may experience higher rates as a result of economic challenges or monetary policy adjustments. For example, countries with robust housing markets and low inflation may offer more competitive mortgage rates than those with higher inflation or economic instability.

Understanding these international variations can help homebuyers gain a broader perspective on interest rate dynamics and consider potential opportunities for cross-border real estate investments. Staying informed about global economic trends and their impact on interest rates can enhance decision-making for prospective homeowners and investors alike.

Can We Predict Future Interest Rates?

Predicting future interest rates is challenging, as they are influenced by a complex interplay of economic, political, and market factors. While economists and financial analysts use various models and indicators to forecast interest rate trends, uncertainties and unexpected events can lead to deviations from predictions.

Key indicators that analysts consider when predicting interest rates include economic growth, inflation, employment data, and central bank policies. By monitoring these factors and staying informed about global economic developments, potential homebuyers can gain insights into possible future rate movements.

While predictions can provide valuable guidance, it's essential for homebuyers to remain flexible and prepared for potential rate changes. Consulting with financial advisors and staying informed about current economic conditions can help borrowers make informed decisions and navigate the mortgage process effectively.

Expert Advice on Navigating Interest Rates

Seeking expert advice is a valuable step for homebuyers looking to navigate the complexities of interest rates and secure favorable mortgage terms. Financial advisors, mortgage brokers, and real estate professionals can provide insights and guidance tailored to individual circumstances.

Experts can help homebuyers understand the factors influencing interest rates, assess the impact on affordability, and explore strategies for managing borrowing costs. They can also assist in comparing lender offers, choosing between fixed and adjustable rates, and timing mortgage applications to align with market conditions.

By leveraging expert advice, homebuyers can make informed decisions, optimize their mortgage terms, and achieve their homeownership goals with confidence.

Frequently Asked Questions

- What is the average home interest rate? The average home interest rate refers to the typical rate borrowers can expect to pay on a mortgage, influenced by various economic factors and lender policies.

- How often do interest rates change? Interest rates can change frequently based on economic conditions, central bank policies, and market dynamics. It's essential to stay updated on current trends.

- Can I negotiate my mortgage interest rate? Yes, borrowers can negotiate interest rates with lenders by comparing offers, improving their credit score, and demonstrating financial stability.

- Is a lower interest rate always better? While a lower interest rate reduces borrowing costs, it's essential to consider other loan terms, such as fees and prepayment penalties, to determine the overall value of the offer.

- How does a rate lock work? A rate lock is an agreement with a lender to secure a specific interest rate for a set period, protecting the borrower from potential rate increases before closing the loan.

- What should I do if interest rates rise after I've applied for a mortgage? If rates rise after applying, borrowers can explore options such as locking in the current rate, renegotiating terms, or considering adjustable-rate mortgages to manage costs.

Conclusion

The average home interest rate is a crucial factor in the homebuying process, influencing affordability, borrowing costs, and financial planning. By understanding the factors that impact interest rates, such as economic conditions, monetary policy, and credit scores, prospective homeowners can make informed decisions and navigate the mortgage market effectively.

Staying informed about current trends, comparing lender rates, and seeking expert advice are essential steps for securing favorable loan terms and achieving homeownership goals. As interest rates continue to fluctuate, homebuyers should remain proactive, adaptable, and well-informed to optimize their mortgage experience and make sound financial choices.

You Might Also Like

Ultimate Guide To Shin-Ōsaka Station: Gateway To Osaka's WondersCherries Benefits: A Sweet Powerhouse For Health

Pelham 123: Intrigue And Drama In The Heart Of New York

Delving Into The Rich Legacy Of Dona Maria: A Cultural Icon

Silica: The Essential Mineral - What You Need To Know

Article Recommendations

- Shirley Jones A Timeless Icon Of Film And Television

- Laura Wrights Children All You Need To Know

- Michael Jackson Through The Years A Legendary Journey