When you purchase an insurance policy, whether it's for your car, home, or health, you're often given the option to choose a deductible amount. This amount is predetermined and agreed upon at the inception of your policy. The relationship between deductibles and premiums is inversely proportional; a higher deductible typically results in lower premiums, whereas a lower deductible leads to higher premiums. This means if you choose a higher deductible, you could save money on monthly premiums but would have to pay more out of pocket if you need to file a claim. Understanding the intricacies of insurance deductibles can sometimes feel overwhelming. However, breaking it down into manageable parts can clarify how deductibles affect your financial responsibilities in the event of a claim. By the end of this article, you'll have a comprehensive understanding of what an insurance deductible is, how it works, and its impact on your overall insurance strategy. This knowledge will empower you to select the deductible level that best aligns with your financial situation and insurance needs.

| Topic | Description |

|---|---|

| Definition | Explains what an insurance deductible is |

| Purpose | Outlines the role of deductibles in insurance policies |

| Types of Deductibles | Describes different deductible structures |

| Choosing a Deductible | Factors to consider when selecting a deductible |

| Impact on Premiums | How deductibles affect insurance premiums |

| Claim Process | Steps to file a claim involving a deductible |

| Common Misconceptions | Addresses myths about deductibles |

| Health Insurance Deductibles | Specifics of deductibles in health insurance |

| Auto Insurance Deductibles | Details of deductibles in auto insurance |

| Home Insurance Deductibles | Deductible specifics in home insurance |

| Pros and Cons | Advantages and disadvantages of deductibles |

| FAQs | Answers to common questions about deductibles |

| Conclusion | Wraps up the discussion on deductibles |

What is the Purpose of an Insurance Deductible?

Insurance deductibles serve several key functions within an insurance policy. Firstly, they help to prevent small claims that can be costly to process for insurers, thereby keeping insurance costs lower for everyone. By requiring policyholders to pay an initial amount out of pocket, insurance companies can focus their resources on more significant claims. This practice reduces administrative costs and discourages frivolous claims, thereby promoting a more efficient insurance system.

Secondly, deductibles create a financial partnership between the insurer and the insured. The policyholders are encouraged to practice due diligence in protecting their insured assets, knowing that they will have to cover a portion of any loss. This shared responsibility helps to reduce the frequency of claims, as policyholders are more likely to take preventative measures to avoid incurring out-of-pocket expenses.

Lastly, deductibles act as a financial buffer for insurers. In catastrophic scenarios where numerous claims are filed simultaneously, such as natural disasters, the deductible ensures that policyholders share some of the financial burden. This arrangement helps insurers manage their financial risk and maintain solvency, ensuring they can meet their obligations to all policyholders.

What Are the Different Types of Deductibles?

Not all deductibles are created equal, and understanding the different types can help you make an informed choice when selecting your insurance policy. Here are some common deductible structures you may encounter:

Fixed Dollar Deductible

This is the most straightforward type of deductible, where a fixed dollar amount is set at the beginning of the policy term. The policyholder must pay this amount before the insurer covers any remaining costs. For example, if you have a $500 deductible on your auto insurance policy and incur $2,000 in damages, you would pay the first $500, and the insurer would cover the remaining $1,500.

Percentage-Based Deductible

Percentage-based deductibles are often found in home insurance policies, especially in regions prone to natural disasters. Instead of a fixed dollar amount, the deductible is calculated as a percentage of the insured value of the property. For instance, if your home is insured for $200,000 and your deductible is 2%, you would pay $4,000 before the insurance coverage kicks in.

Aggregate Deductible

An aggregate deductible applies across multiple claims within a policy period. This type is common in health insurance policies. Once the cumulative amount of your out-of-pocket expenses reaches the aggregate deductible limit, the insurer covers all subsequent claims for the remainder of the policy term. This structure benefits policyholders with multiple claims, as they only need to meet the deductible once per period.

Per-Incident Deductible

As the name suggests, a per-incident deductible applies to each separate claim filed. This means that policyholders must pay the deductible amount each time they file a claim, regardless of whether they have already met the deductible for previous claims. This structure is common in auto insurance policies and encourages policyholders to minimize the number of claims filed.

How to Choose the Right Deductible for You?

Choosing the right deductible involves balancing your financial situation with your risk tolerance. Here are some factors to consider when selecting a deductible:

- Financial Situation: Assess your current financial status and determine how much you can comfortably afford to pay out of pocket in the event of a claim. If you have a healthy emergency fund, a higher deductible may be a feasible option to reduce your premiums.

- Risk Tolerance: Consider your willingness to assume financial risk. If you're risk-averse, a lower deductible may provide peace of mind, even if it means higher premiums.

- Asset Value: Evaluate the value of the asset you're insuring. For high-value assets, a lower deductible might be wise to ensure you're adequately covered in the event of a loss.

- Claim Frequency: Consider the likelihood of filing a claim. If you anticipate frequent claims, a lower deductible could be more cost-effective in the long run.

Ultimately, the right deductible is one that aligns with your financial goals and risk tolerance while providing the protection you need.

How Do Deductibles Impact Insurance Premiums?

The relationship between deductibles and premiums is inversely proportional. A higher deductible reduces the insurer's risk, resulting in lower premiums for the policyholder. Conversely, a lower deductible increases the insurer's risk, leading to higher premiums.

Here's how this relationship plays out:

- High Deductible, Low Premium: Opting for a high deductible means you're willing to take on more financial responsibility in the event of a claim. As a result, insurers offer lower premiums as they have less risk exposure.

- Low Deductible, High Premium: Choosing a low deductible reduces your out-of-pocket expenses when filing a claim. However, insurers compensate for the increased risk by charging higher premiums.

It's important to calculate the potential savings from lower premiums against the increased out-of-pocket costs associated with a higher deductible. This analysis can help you determine the most cost-effective deductible level for your needs.

What Is the Claim Process Involving a Deductible?

Filing an insurance claim involves several steps, and understanding the role of your deductible is crucial for a smooth process. Here's how it typically works:

- Assess the Damage: After an incident, assess the extent of the damage or loss to determine whether it warrants filing a claim. If the damage is minor and the repair cost is below or slightly above your deductible, you may opt to cover the expenses out of pocket to avoid affecting your claims history.

- File the Claim: If you decide to proceed with a claim, contact your insurer to initiate the process. Provide all necessary documentation, including photos, receipts, and a detailed description of the incident.

- Pay the Deductible: Once your claim is approved, you'll be required to pay your deductible amount. This payment is typically made directly to the service provider or deducted from the total payout you receive from the insurer.

- Receive Compensation: After the deductible is paid, the insurer will cover the remaining costs, up to the policy limits. Ensure you understand any policy exclusions or limitations that may affect your compensation.

Being familiar with the claim process can help streamline your experience and ensure prompt resolution of your claim.

Common Misconceptions About Insurance Deductibles

Insurance deductibles can be confusing, leading to several misconceptions. Let's address some of the most common myths:

Myth 1: Deductibles are the Same for All Policies

This is not true. Deductibles vary depending on the type of insurance and the specifics of each policy. For example, health insurance may have different deductible structures compared to auto or home insurance.

Myth 2: Paying a Deductible Guarantees Full Coverage

While paying your deductible is a prerequisite for insurance coverage, it doesn't guarantee that all costs will be covered. Policy limits, exclusions, and other factors can affect the final payout.

Myth 3: Deductibles Only Apply to Large Claims

Deductibles apply to any claim, regardless of the size. In fact, they are particularly beneficial in reducing the frequency of small claims, which can increase overall insurance costs.

Myth 4: Higher Deductibles Always Save Money

While higher deductibles can lead to lower premiums, they may not always result in overall savings. Consider the potential out-of-pocket costs and your financial situation before opting for a higher deductible.

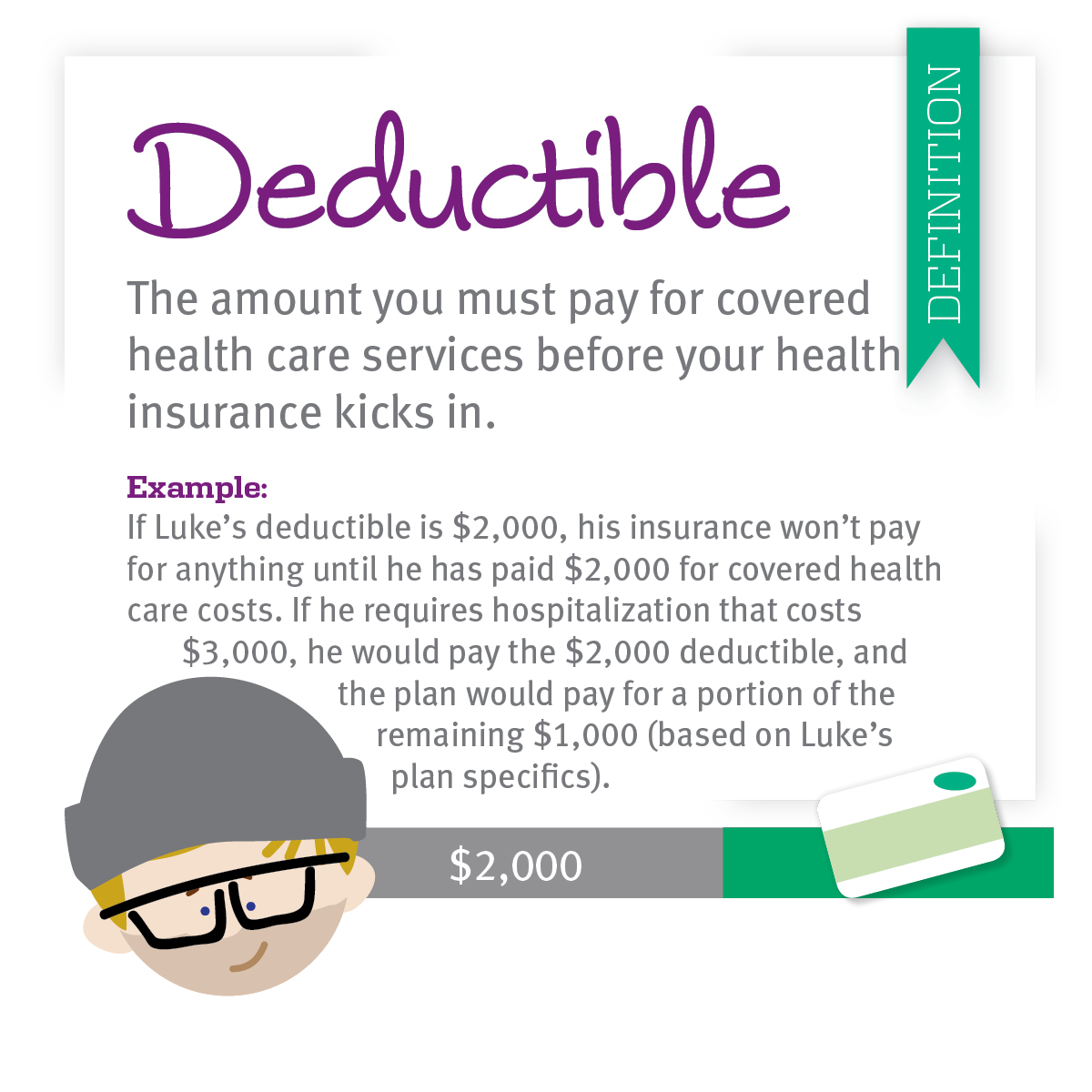

What Are Health Insurance Deductibles and How Do They Work?

Health insurance deductibles are a critical component of many healthcare plans. They represent the amount you pay for covered healthcare services before your insurance plan starts to pay. Here's how they typically work:

- Individual vs. Family Deductibles: Health insurance plans may have separate deductibles for individuals and families. An individual deductible applies to each person covered by the plan, while a family deductible applies collectively to all family members.

- In-Network vs. Out-of-Network Deductibles: Many health plans have different deductibles for services received from in-network and out-of-network providers. In-network providers usually have lower deductibles and copayments.

- Preventive Services: Under many health plans, preventive services such as vaccinations and screenings are covered without requiring you to meet the deductible.

Understanding your health insurance deductible is crucial for managing your healthcare costs effectively.

How Do Auto Insurance Deductibles Work?

Auto insurance deductibles apply to various types of coverage, including collision and comprehensive insurance. Here's how they function:

- Collision Coverage: This deductible applies when your vehicle is damaged due to a collision with another vehicle or object. You pay the deductible amount, and the insurer covers the remaining repair costs.

- Comprehensive Coverage: Comprehensive coverage applies to non-collision-related damages, such as theft, vandalism, or natural disasters. You pay the deductible, and the insurer covers the rest.

- Glass Coverage: Some auto policies include a separate deductible for glass damage. However, many insurers offer full coverage for glass repair or replacement without a deductible.

Choosing the right deductible for your auto insurance can help you balance premium costs with potential out-of-pocket expenses.

What Role Do Deductibles Play in Home Insurance?

Home insurance deductibles are an essential part of protecting your property. Here's how they typically work:

- Standard Deductible: Most home insurance policies have a standard deductible for perils such as fire, theft, and vandalism. You pay the deductible, and the insurer covers the remaining costs.

- Percentage-Based Deductibles: In areas prone to natural disasters, insurers may impose percentage-based deductibles for specific perils like hurricanes or earthquakes.

- Special Deductibles: Some policies include special deductibles for high-value items, such as jewelry or artwork. These deductibles may be higher or lower than the standard deductible.

Understanding your home insurance deductible can help you make informed decisions about your coverage and financial responsibilities.

What Are the Pros and Cons of Insurance Deductibles?

Insurance deductibles offer several advantages and disadvantages:

Pros

- Lower Premiums: Higher deductibles can lead to lower premiums, making insurance more affordable.

- Reduced Small Claims: Deductibles discourage small claims, promoting a more efficient insurance system.

- Shared Responsibility: Deductibles create a financial partnership between insurers and policyholders, encouraging asset protection.

Cons

- Increased Out-of-Pocket Costs: Higher deductibles mean more significant out-of-pocket expenses when filing a claim.

- Potential Financial Strain: Inadequate planning for deductible expenses can lead to financial strain in the event of a claim.

- Complexity: Understanding different deductible structures can be confusing for policyholders.

Weighing the pros and cons of deductibles can help you make informed decisions about your insurance coverage.

FAQs About Insurance Deductibles

1. What is an insurance deductible?

An insurance deductible is the amount you pay out of pocket before your insurance coverage begins. It applies to various types of insurance, including health, auto, and home insurance.

2. How does a deductible affect my insurance premium?

The relationship between deductibles and premiums is inversely proportional. A higher deductible usually results in lower premiums, while a lower deductible leads to higher premiums.

3. Can I change my deductible after purchasing a policy?

Yes, you can often change your deductible during your policy's renewal period. However, changing your deductible may affect your premium, so it's essential to discuss options with your insurer.

4. Do all insurance policies have deductibles?

Not all insurance policies have deductibles. Some policies, like life insurance, typically do not include deductibles. However, most health, auto, and home insurance policies do have deductibles.

5. What happens if my claim is less than the deductible?

If your claim amount is less than your deductible, you will be responsible for covering the entire cost out of pocket. The insurance company will not contribute to expenses below the deductible threshold.

6. Are there ways to reduce my deductible?

Some insurers offer optional coverage or endorsements that can reduce or eliminate deductibles for specific claims. Additionally, maintaining a good claims history and bundling policies may provide opportunities for deductible reductions.

Conclusion

Understanding insurance deductibles is essential for making informed decisions about your insurance coverage. By knowing how deductibles work, their impact on premiums, and the various types available, you can select the right deductible that aligns with your financial situation and risk tolerance. Deductibles play a crucial role in the insurance industry, promoting shared responsibility and efficient claim processes while helping policyholders manage their insurance costs effectively. Armed with this knowledge, you can confidently navigate the complexities of deductibles and optimize your insurance strategy to meet your needs.

For further reading on insurance policies and their intricacies, consider exploring resources from reputable financial advisory organizations or the Insurance Information Institute.

You Might Also Like

Mastering The Art Of Shaving: Norelco Shaver RevealedDeep Dive Into Thought Provoking Questions For Insightful Conversations

Clear That Stuffy Nose: Effective Tips And Techniques

Is Berberine Bad For Kidneys? Unveiling Health Impacts

Top Choices For Optimal Hydration: The Best Drinks Explained

Article Recommendations

- Meet The Talented Actor Behind Joe Goldberg Exploring The Stars Career And Role

- Unveiling The Mystery Of Tom Burke Wife Everything You Need To Know

- Tom Welling Young A Stars Early Days And Rise To Fame

.png/9025a687-d4ba-450f-fa19-12a92c3cb212?t=1637254391104&imagePreview=1)