Choosing between a Roth 401k and a Roth IRA can be daunting, but it's a critical step in ensuring a financially secure future. Each type of account has unique features that cater to different financial situations. While both offer tax-free growth and withdrawals in retirement, they differ in terms of contribution limits, employer matching, and income eligibility. Understanding these differences will empower you to maximize your savings and optimize your retirement plan.

With the increasing complexity of retirement planning, it's more important than ever to evaluate your options carefully. This comprehensive guide will delve into the specifics of Roth 401k and Roth IRA accounts, helping you make an educated choice. By comparing their benefits, limitations, and how they fit into your overall financial picture, you'll be better equipped to secure your financial future and enjoy a comfortable retirement. Let's explore the intricacies of Roth 401k vs Roth IRA and discover how each can work for you.

Table of Contents

- What is a Roth 401k?

- What is a Roth IRA?

- Key Differences Between Roth 401k and Roth IRA

- How Does a Roth 401k Work?

- How Does a Roth IRA Work?

- Advantages of a Roth 401k

- Advantages of a Roth IRA

- Disadvantages of a Roth 401k

- Disadvantages of a Roth IRA

- Which is Better for You?

- Roth 401k vs Roth IRA Contribution Limits

- Tax Benefits of Roth 401k and Roth IRA

- Impact of Employer Matching

- Frequently Asked Questions

- Conclusion

What is a Roth 401k?

The Roth 401k is an employer-sponsored retirement savings plan that combines features of a traditional 401k with those of a Roth IRA. Contributions are made with after-tax dollars, meaning you pay taxes upfront, but qualified withdrawals during retirement are tax-free. This structure is particularly advantageous for individuals who expect to be in a higher tax bracket during retirement or those who prefer tax-free income later in life.

Roth 401k accounts were introduced in 2006 to offer more flexibility and tax benefits to employees saving for retirement. Unlike a traditional 401k, where contributions are tax-deductible, Roth 401k contributions do not reduce your taxable income for the year. Instead, they provide tax-free growth and withdrawals, an attractive feature for many retirement savers.

Employers offering a Roth 401k often include matching contributions, although these matches are made on a pre-tax basis and held in a separate traditional 401k account. This means the matched funds will be taxed upon withdrawal. The combination of Roth and traditional contributions allows for diversified tax treatment and can be a strategic component of a comprehensive retirement plan.

What is a Roth IRA?

A Roth IRA is an individual retirement account that allows for after-tax contributions, offering tax-free growth and withdrawals. Unlike the Roth 401k, a Roth IRA is not tied to an employer and can be established by anyone with earned income, subject to income limits. This independence makes it a flexible option for individuals seeking to manage their retirement savings outside of employer plans.

Introduced in 1997, Roth IRAs provide significant tax advantages for retirement savers. Contributions are made with after-tax dollars, similar to a Roth 401k, allowing for tax-free withdrawals in retirement. However, Roth IRAs are subject to income eligibility limits, and higher earners may not qualify for direct contributions.

One of the appealing features of a Roth IRA is the flexibility in withdrawal rules. Contributions can be withdrawn at any time without penalties or taxes, providing liquidity and accessibility. This feature makes Roth IRAs particularly attractive for individuals seeking a balance between long-term savings and financial flexibility.

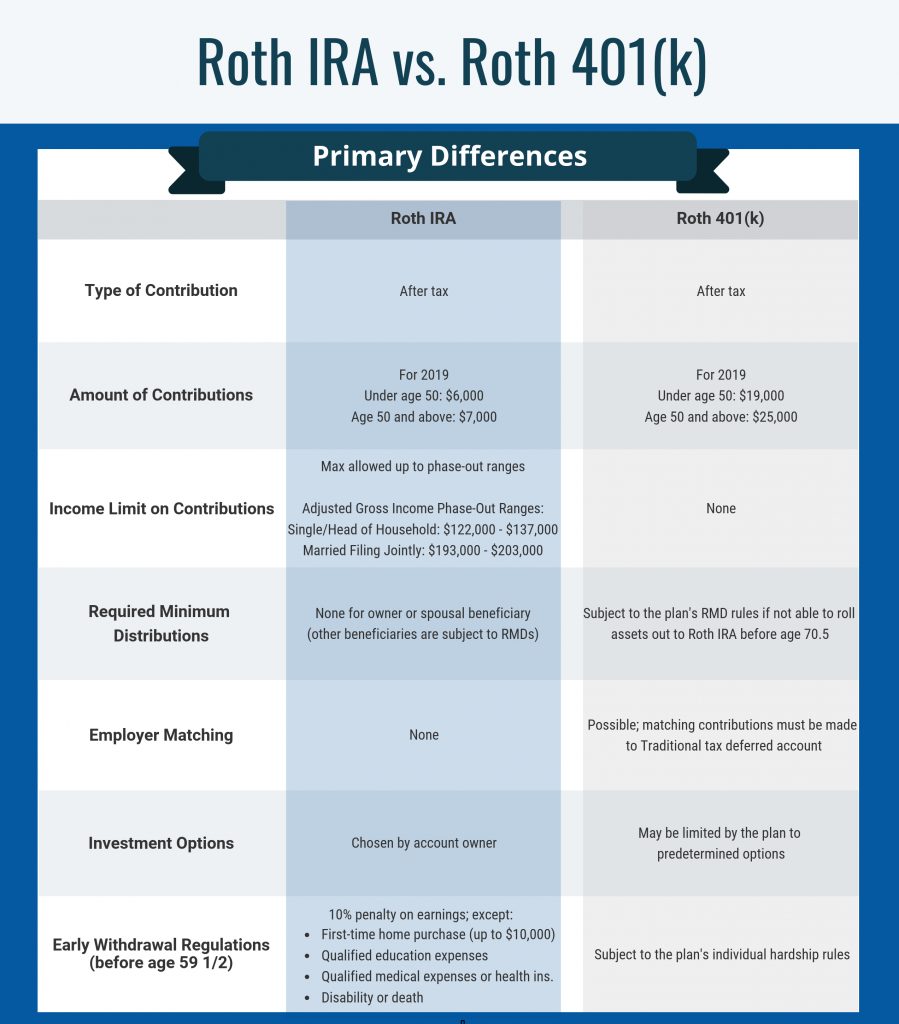

Key Differences Between Roth 401k and Roth IRA

While both Roth 401k and Roth IRA accounts offer tax-free growth and withdrawals, they differ in several key areas:

- Contribution Limits: Roth 401k accounts have higher contribution limits compared to Roth IRAs, allowing for more substantial annual savings.

- Income Limits: Roth IRAs have income eligibility restrictions, whereas Roth 401k accounts do not have such limitations, making them accessible to a broader range of earners.

- Employer Matching: Roth 401k plans may include employer matching contributions, enhancing the growth potential of your retirement savings.

- Required Minimum Distributions (RMDs): Roth 401k accounts require RMDs starting at age 72, while Roth IRAs do not, allowing for more flexibility in managing retirement distributions.

Understanding these differences is critical for tailoring your retirement strategy to your financial situation and goals. Both accounts offer unique advantages that can complement each other when used strategically.

How Does a Roth 401k Work?

A Roth 401k functions similarly to a traditional 401k but with distinct tax treatment. Employees contribute after-tax dollars, which means they pay taxes on the contributions during the current tax year. The advantage of this approach is that withdrawals of contributions and earnings are tax-free during retirement, provided certain conditions are met.

To contribute to a Roth 401k, you must be employed by an employer that offers this type of retirement plan. Contributions are typically deducted from your paycheck on a post-tax basis, and you have the flexibility to choose your contribution level within the annual limits set by the IRS.

Roth 401k accounts are subject to required minimum distributions (RMDs) starting at age 72, unless you are still employed with the company offering the plan. This requirement is an essential consideration for retirement planning, as it impacts your withdrawal strategy and tax planning.

How Does a Roth IRA Work?

A Roth IRA operates independently of employer-sponsored plans, allowing individuals to contribute after-tax dollars to an account that grows tax-free. Withdrawals of contributions are tax-free at any time, and earnings can be withdrawn without penalties or taxes once the account holder reaches age 59½ and has held the account for at least five years.

Roth IRAs have annual contribution limits, which are lower than those for Roth 401k accounts. Additionally, eligibility to contribute directly to a Roth IRA is subject to income limits, which can affect high earners' ability to contribute.

The absence of required minimum distributions (RMDs) is a significant advantage of Roth IRAs, allowing account holders to let their investments grow tax-free for as long as they wish. This flexibility can be particularly beneficial for estate planning and managing retirement income.

Advantages of a Roth 401k

Roth 401k accounts offer several advantages for retirement savers:

- Higher Contribution Limits: Roth 401k accounts allow for higher annual contributions compared to Roth IRAs, enabling more substantial savings.

- Tax-Free Withdrawals: Qualified withdrawals of contributions and earnings are tax-free, providing predictable tax treatment during retirement.

- Employer Matching: Many employers offer matching contributions, which can significantly boost your retirement savings.

- No Income Limits: Unlike Roth IRAs, Roth 401k accounts do not have income restrictions, making them accessible to all earners.

These advantages make Roth 401k accounts a powerful tool for building a robust retirement portfolio, particularly for individuals expecting to be in higher tax brackets during retirement.

Advantages of a Roth IRA

Roth IRAs provide several benefits for retirement planning:

- Tax-Free Growth: Contributions and earnings grow tax-free, with tax-free withdrawals in retirement.

- Flexibility: Contributions can be withdrawn at any time without penalties, providing financial flexibility.

- No RMDs: Roth IRAs do not require minimum distributions, allowing for continued tax-free growth beyond age 72.

- Estate Planning Benefits: Roth IRAs can be passed to heirs without immediate tax implications, making them a valuable estate planning tool.

These benefits make Roth IRAs an attractive option for individuals seeking flexibility and long-term growth potential in their retirement savings.

Disadvantages of a Roth 401k

While Roth 401k accounts offer significant advantages, they also have some drawbacks:

- Required Minimum Distributions: Roth 401k accounts are subject to RMDs starting at age 72, which can limit tax-free growth.

- Employer Plan Limitations: Access to a Roth 401k is contingent on employer offerings, and plan options may be limited.

- Tax Implications on Employer Matches: Employer matching contributions are made to a separate traditional 401k account, which is subject to taxes upon withdrawal.

Considering these disadvantages is essential for developing a balanced retirement strategy that addresses potential limitations and maximizes benefits.

Disadvantages of a Roth IRA

Roth IRAs, while beneficial, have some limitations:

- Income Limits: Contribution eligibility is restricted by income limits, potentially excluding high earners from direct contributions.

- Lower Contribution Limits: Roth IRAs have lower annual contribution limits compared to Roth 401k accounts, which can restrict savings potential.

These disadvantages highlight the importance of evaluating your financial situation and goals when choosing between Roth IRA and other retirement savings options.

Which is Better for You?

The choice between a Roth 401k and a Roth IRA depends on various factors, including your income level, retirement goals, and financial situation. Here are some considerations to help guide your decision:

- Income Level: If your income exceeds the limits for Roth IRA contributions, a Roth 401k may be a more suitable option.

- Employer Matching: If your employer offers a Roth 401k with matching contributions, it can significantly boost your retirement savings.

- Flexibility: If you value flexibility in withdrawal options and want to avoid RMDs, a Roth IRA may be more appealing.

- Contribution Capacity: If you want to maximize your annual contributions, a Roth 401k's higher limits may be advantageous.

Ultimately, the decision should align with your long-term financial goals and tax strategy. Consider consulting a financial advisor to explore which option best suits your needs.

Roth 401k vs Roth IRA Contribution Limits

Understanding the contribution limits of Roth 401k and Roth IRA accounts is crucial for effective retirement planning. Here are the key differences:

- Roth 401k Contribution Limits: As of 2023, individuals can contribute up to $22,500 annually to a Roth 401k, with an additional catch-up contribution of $7,500 for those aged 50 and older.

- Roth IRA Contribution Limits: The annual contribution limit for Roth IRAs is $6,000, with a catch-up contribution of $1,000 for individuals aged 50 and older.

The higher contribution limits of Roth 401k accounts provide an opportunity for more aggressive savings, which can be beneficial for individuals with higher income levels or those looking to maximize their retirement fund growth.

Tax Benefits of Roth 401k and Roth IRA

Both Roth 401k and Roth IRA accounts offer significant tax advantages that can impact your retirement strategy:

- Roth 401k Tax Benefits: Contributions are made with after-tax dollars, providing tax-free withdrawals of both contributions and earnings. Employer matches are pre-tax and grow tax-deferred until withdrawal.

- Roth IRA Tax Benefits: Contributions grow tax-free, and withdrawals of contributions and earnings are tax-free if the account has been open for at least five years and the account holder is 59½ or older.

These tax benefits can significantly enhance your retirement savings by reducing your tax liability during retirement and allowing for more predictable financial planning.

Impact of Employer Matching

Employer matching contributions can play a significant role in the growth of your retirement savings when investing in a Roth 401k:

- Boosting Savings: Employer matches can increase the total contributions to your retirement account, accelerating the growth of your retirement fund.

- Tax Treatment: While employer matches are made on a pre-tax basis and are held in a traditional 401k account, they still provide a valuable supplement to your retirement savings.

Understanding the terms of your employer's matching program and maximizing your contributions to take full advantage of this benefit can significantly impact your long-term financial security.

Frequently Asked Questions

What is the main difference between Roth 401k and Roth IRA?

The main difference lies in contribution limits and income eligibility. Roth 401k accounts have higher contribution limits and no income restrictions, while Roth IRAs have lower contribution limits and income eligibility requirements.

Can I contribute to both a Roth 401k and a Roth IRA?

Yes, you can contribute to both accounts if you meet the eligibility requirements and adhere to the respective contribution limits.

Are employer matches in a Roth 401k also Roth contributions?

No, employer matches are made on a pre-tax basis and are held in a separate traditional 401k account, subject to taxes upon withdrawal.

Do Roth IRA accounts have required minimum distributions?

No, Roth IRA accounts do not require minimum distributions, allowing for continued tax-free growth and greater flexibility in retirement planning.

What happens if I exceed the income limits for a Roth IRA?

If you exceed the income limits for a Roth IRA, you may be eligible to contribute to a Roth 401k if offered by your employer, or explore a backdoor Roth IRA strategy with the help of a financial advisor.

Can I withdraw contributions from a Roth IRA at any time?

Yes, you can withdraw contributions from a Roth IRA at any time without penalties or taxes, providing flexibility and accessibility to your funds.

Conclusion

Deciding between a Roth 401k and a Roth IRA is a significant step in crafting a successful retirement strategy. Each account offers unique benefits and limitations that cater to different financial needs and goals. By understanding these distinctions and evaluating how they align with your personal circumstances, you can make informed decisions to optimize your retirement savings.

Whether you choose a Roth 401k, a Roth IRA, or a combination of both, it's essential to consider factors such as contribution limits, tax benefits, and employer matching. Consulting with a financial advisor can provide valuable insights and help tailor your retirement plan to ensure you achieve long-term financial security and enjoy a comfortable retirement.

As you navigate the complexities of retirement planning, remember that both Roth 401k and Roth IRA accounts offer powerful tools for building a solid financial foundation. With careful consideration and strategic planning, you can harness the benefits of these accounts to secure a prosperous and fulfilling future.

Learn more about Roth 401k vs Roth IRAYou Might Also Like

All About Keyboard Symbols: Their Uses And MeaningsFinding The Best Child Psychiatrist Near Me: A Comprehensive Guide

Maximizing Your Workout: The Benefits Of An LA Fitness Membership

How Long Does A Spray Tan Last? Your Complete Guide

Star Wars In Movies: A Cinematic Phenomenon

Article Recommendations

- Unveiling The Mystery Of Tom Burke Wife Everything You Need To Know

- Exploring The World Of Mkvmoviespoint Everything You Need To Know

- Meet The Talented Actor Behind Joe Goldberg Exploring The Stars Career And Role